solely $22.50 shipped!")

")

Podcast: Play in new window | Obtain

The Fed made very clear this week its intentions to start easing its long-standing apply of pumping cash into the U.S. Financial system. This implies they wish to push rates of interest up on the broader economic system–a day many people have been awaiting.

A whole lot of issues will include larger rates of interest, however one main adverse everyone seems to be bracing for is the upper price to borrow cash. This may–theoretically–influence money worth life insurance coverage insurance policies. Not less than these utilizing a variable mortgage rate of interest.

In order charges tick up this yr, will these of you with excellent coverage loans be paying extra curiosity over the yr? The quick reply might be not. This mentioned, now is a superb time to re-visit the topic of coverage loans within the tactical sense.

Variable Loans and Their Widespread Pegged Index

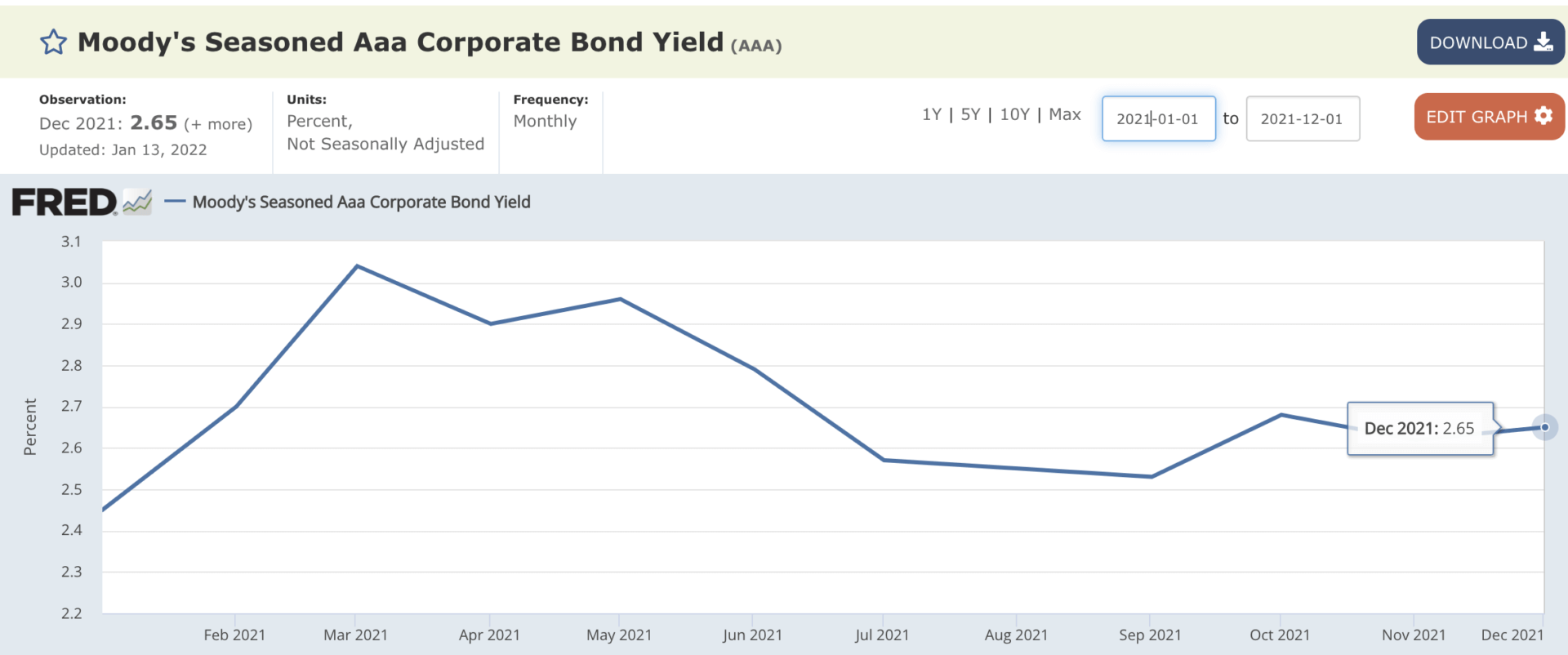

Most insurance coverage contracts with variable loans–at the very least in the entire life area–peg the mortgage fee to the Moody’s Company Bond Index. These contracts additionally often embody a succession plan ought to this index stop to exist.

As of January of 2022, the index sits at 2.65%.

Most complete life insurance policies don’t permit the mortgage fee charged on coverage loans to fall beneath the assured accumulation fee of the coverage–the truth is most place a diffusion between the assure accumulation fee and the minimal mortgage rate of interest.

On common, the minimal mortgage fee for these variable loans is 100 foundation factors above the assured accumulation fee. Which means that for a lot of insurance policies in existence, the minimal mortgage fee is 5%–this assumes insurance policies issued underneath a 4% minimal assure, which was the norm till the start of 2022.

With mortgage charges usually sitting at 5% and the Moody’s Index at 2.65%, we’ve plenty of floor to cowl earlier than life insurance coverage coverage loans expertise a rise in rate of interest. Whereas it is totally potential that Fed exercise will ultimately get us there, I would not predict rates of interest rising that far that quick inside the yr.

However What Occurs if We Do Get There?

If inflation continues to be a bee in Jerome Powell’s bonnet, it is potential we discover out selves in a world, the place the Moody’s Index does surpass 5%. On this state of affairs, it is completely potential that mortgage charges on these insurance policies will increase. However, nothing takes place in a vacuum.

Rising rates of interest additionally give energy to the probability of rising dividend charges. As soon as insurers can purchase bonds with larger yields, funding earnings will rise. This improve in funding earnings will produce a constructive motion in dividends.

I might predict that attending to an rate of interest setting the place the Moody’s Index is larger sufficient to trigger a rise in these variable loans may even be an setting able to producing larger dividend rates of interest on complete life insurance coverage merchandise.

Direct Recognition Seemingly Has an Benefit Right here

Whereas I nonetheless do not consider that dividend recognition has an absolute benefit no matter which technique is practiced, sharply rising rates of interest that trigger mortgage charges to leap earlier than company-wide dividend charges do might not be as huge an issue for direct recognition contracts.

Since most direct recognition contracts peg the dividend payable on money values that again a mortgage to the mortgage rate of interest, a rising mortgage rate of interest will probably improve the dividends payable as nicely.

We have been Planning for This

We have been planning for larger rates of interest for over a decade. A part of our product choice course of included how merchandise behaved underneath an array of situations, and rising rates of interest has at all times been a top-of-mind circumstance.

We have lengthy held the opinion that contract provisions matter–it is why we do not get hung up in foolish meaningless particulars like dividend recognition simply in and of itself. The suggestions we have made over time took the potential of rising charges, and the influence it might have on coverage loans under consideration, and we’re fairly satisfied that we’ve a stable technique for this.