")

")

Ihor Martsenyuk/iStock via Getty Images

About the company

Ferrexpo (OTCPK:FEEXF) is the third largest exporter of iron ore pellets in the world with its main operations located in Ukraine. Ferrexpo has vertically integrated operations from iron ore mining through iron ore concentrate and pellet production and subsequent logistics. The company extracts iron ore in central Ukraine in the region of Poltava approximately 350 kilometers away from the battlefield. The company produces high grade (65% FE and higher) iron ore pellets, which play a critical role in decarbonization efforts of steel making industry.

Investment thesis

Ferrexpo seems like a valuation play as investors are mispricing the company’s assets due to ongoing war. The company is mispriced either using the balance sheet approach or using the income valuation approach, through its ability to generate future cash flows. Ferrexpo has no debt, so it can’t default. It has a solid history of capital allocation, regularly paying dividends to its investors. Finally, the steel industry in general and especially in Europe won’t be able to achieve its decarbonization goals without improving its carbon heavy processes. Using high grade iron ore pellets in steel production is one of the main components in achieving these goals. The investment in Ferrexpo has always required a certain discount to its fair value due to its status as an emerging market company with shaky corporate governance. However, I believe that the current market value does not correctly reflect the intrinsic value of the company and patient investors should be able to generate solid returns buying the stock at these rock bottom prices.

Bloomberg

Market environment

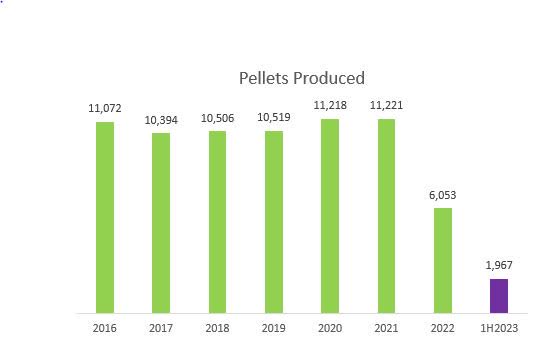

In 2022, the global pellet export market represented approximately 111 million tons, of which Ferrexpo produced6.1 million tons, which gives it a global market share of 5.6%. In 2022, the annual production was severely impacted by electricity blackouts and operational slowdowns as a result of the ongoing war. Decrease in production stabilized in 1H 2023, when pellets produced reached 2.0 million tons, which was 57% increase compared to 2H 2022. Historically, Ferrexpo had annual capacity above 10 million tons, which gives it an opportunity to increase its production once the war ends. Even though it is not possible to predict the development of the war, the management of the company stated that in 2025, they expect to produce volumes closer to average production. It is expected that the overall size of the pellet export market will revert to a similar size as seen in recent years, which is approximately 130 million tons. In terms of pricing of pellet production, a significant proportion of sales is arranged via long-term contracts. In 2022, the company had 96% of all sales arranged under long-term agreements, which provides a floor under future revenues, even if the level of production in the following years remained unchanged. Unless the current situation worsens, it seems probable that the company has reached its bottom in pellet production and in revenues generated in the last twelve months. Coincidentally, the level of production also corresponds with the price of the stock, which makes me believe that the stock is very close to its bottom.

Annual reports

Logistics is the key

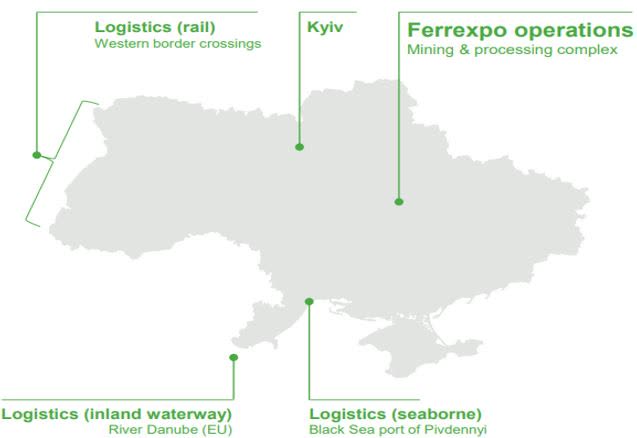

Ferrexpo’s main operations are in the Poltava region of central Ukraine and has not seen any direct combat between Russian and Ukrainian forces. In 2022, 80% of total production was exported to Europe. Central and Eastern Europe will remain the most important markets until the Black Sea routes are open again. The main transport routes are either railways or inland waterways (barging). In 2Q 2023 production report management stated that the company has the capacity to increase production but is constrained in logistics. The company has plans to come up with alternative supply routes in the near future, which supports the idea of higher production and revenues in 2H 2023.

Company presentation

Valuation

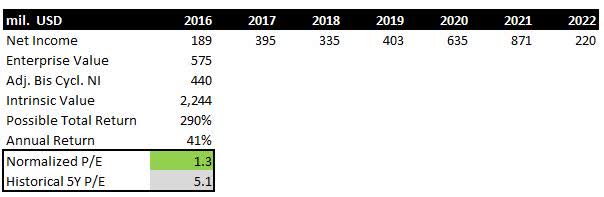

The best time to buy stocks is when nobody wants them. The war in Ukraine is a horrible tragedy on Ukrainian people, but it provides an opportunity to buy assets nobody wants at this time. In Ferrexpo case, two events are happening at the same time. The first visible factor is war. The second less visible event is downturn in commodity cycle, triggered by slowdown in China. Ferrexpo has the ability to withstand both events. It has a solid balance sheet with no debt, and it is still able to generate cash even in the middle of the war. Looking at Ferrexpo in a more standardized way, the company has market capitalization of $680 million and Enterprise Value (Market Cap net cash) is $575 million. The expected consensus FY 2023 earnings are $81 million, which gives it a P/E multiple of 8.1 times. It does not seem like a screaming bargain. However, average normalized earnings across the business cycle are closer to $440 million. This gives us an adjusted P/E multiple of 1.3x and earnings yield of 77%. Both values should provide a reasonable margin of safety for investors. In commodity businesses it is a mistake to use currently depressed earnings due to cyclicality of the business, that’s why using business cycle adjusted earnings are a better fit. The current business cycle in iron pellets production started approximately in 2016 and lasted until 2023, which is compatible with slowdown across the whole industry. Historically, Ferrexpo has traded at 5.1 times earnings. If this multiple is applied to normalized earnings, the intrinsic value of the company should be around $2.2 billion. This gives a potential return of 290% from the current stock price. This return could be achieved if the war subsides, and the global pellet production industry returns to its pre-pandemic state. If the last business cycle should be taken as a benchmark, return to mean could be reached within three to five years. In the case of four years, possible return exceeds 40% per annum.

Own Work

Potential risks

The most urgent risk for Ferrexpo and also for Ukraine is the long war. Even though the company showed the ability to operate in the middle of conflict, the long war would negatively impact the financial position of the company. The management beliefs that in 2025, Ferrexpo should be able to return to its pre-war production, but any prolongation of the war could affect this forecast. The second risk is a significant slowdown in steel demand. As Central and Eastern Europe are primary markets, negative development in CEE economies could have detrimental effects on steel production and subsequent demand for iron pellets.

Summary

This year, Ferrexpo has reached its bottom in production, and it seems highly likely that the bottom in production will correspond with the bottom in its stock price. The company has managed to stabilize its logistics routes to Central and Eastern Europe regardless of the situation in the Black Sea. Net cash on the balance sheet enables the company to withstand period of war and does not impact going concern status of the company. Patient investors willing to look behind the ongoing war and slowdown in the pellet industry could earn a 40% return on an annual basis.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.