Twilio Inc. (NYSE:TWLO) is a reasonably priced inventory. Although paying 12x subsequent yr’s non-GAAP working income looks as if a discount inventory, notably when you think about that just about 15% of its market cap is made up of money, Twilio’s progress prospects have fizzled out.

A mixture of a tricky macro backdrop, whereas the vast majority of Twilio’s revenues are usage-based (web page 12), along with a hyper-competitive surroundings, has meant that Twilio’s progress charges at the moment are scampering across the double-digit figures, and never way more.

In sum, I do not see Twilio as a compelling funding alternative.

Speedy Recap

Again in February, I concluded my impartial evaluation by saying,

Regardless of its enhancing profitability, the inventory’s valuation at 16x ahead non-GAAP working income raises considerations about its enchantment to each progress and worth traders. On this delicate stability, Twilio seems to be in a difficult place, requiring a cautious reassessment of its trajectory. As an investor, the chances appear much less favorable in the mean time, leaving me on the sidelines on Twilio.

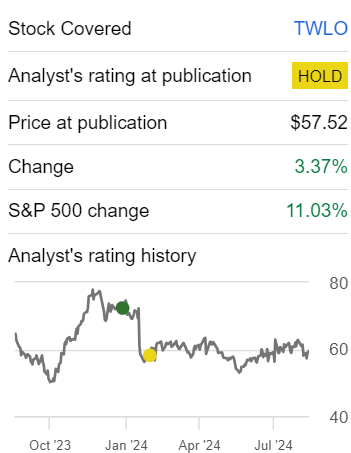

Writer’s work on TWLO

In hindsight, it seems that I made the precise name shifting to the sidelines on TWLO, because the inventory would go on to underperform the S&P 500 (SP500) by mid-single digits over the approaching 6 months. At the moment, as I sit up for subsequent yr, I stay firmly on the sidelines as I query its upside potential.

Twilio’s Close to-Time period Prospects

Twilio offers cloud-based communication providers that allow companies to attach with their clients by way of messaging, voice, e-mail, and video, via APIs (Utility Programming Interfaces).

Its key worth proposition is simplifying how companies combine communication instruments into their apps with no need to construct the infrastructure from scratch. Twilio’s platform helps companies supply personalised, real-time buyer interactions whereas reducing operational bills and growing companies’ buyer engagement.

Within the close to time period, Twilio’s prospects appear steady because it focuses on driving profitability and operational self-discipline. Nevertheless, its progress has been slowing, with income will increase within the single digits in comparison with its earlier greater progress charges.

This deceleration displays a maturing market, alongside macroeconomic uncertainties affecting its usage-based income mannequin. To this finish, as I’ve mentioned on quite a few events, I’ve but to search out many pure-play consumption enterprise fashions which might be successful.

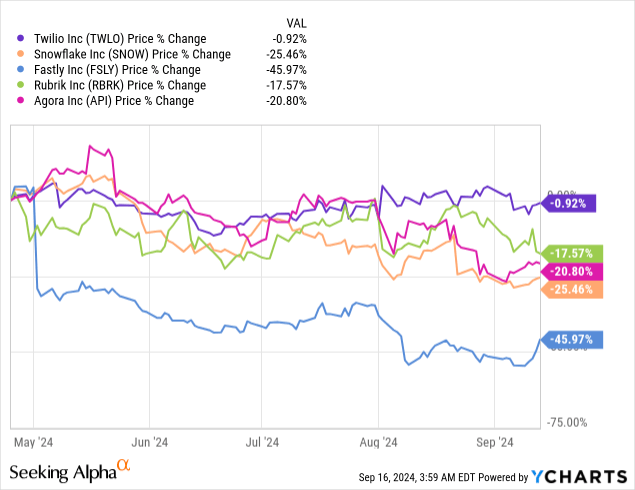

Information by YCharts

This isn’t an unique record of comparable comparable consumption-based enterprise fashions, however moderately a handful of friends, all displaying how their prospects have moderated of late.

What’s extra, Twilio operates in a extremely aggressive area, the place many corporations with sufficient means at the moment are contemplating utilizing AI to construct their very own Software program as a Service, or SaaS, platforms in-house.

Given this background, let’s now talk about its fundamentals.

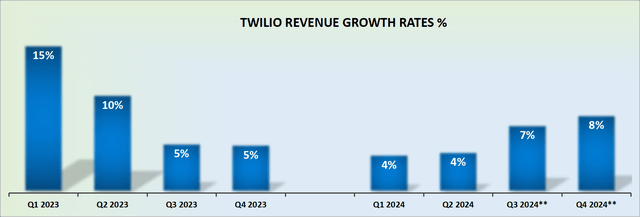

Twilio’s Income Development Charges Depart A lot to be Desired

TWLO income progress charges

Twilio is now not a progress enterprise. It is now a enterprise with a “high-tech narrative” however not one of the fundamentals to assist that narrative.

Investing is a recreation of chances. And it is essential to know that there is not any such factor as a risk-free return.

It is all about wanting on the firm, striving to make assumptions about its future prospects, and pricing in these prospects relative to what the market is anticipating.

Moreover, when the traders appraise Twilio and take into account its potential outcomes for 3 years down the street, I think few traders would critically take into account Twilio as returning to mid-teens progress charges.

Certainly, I think that the almost certainly state of affairs for Twilio is that its progress charges stabilize across the mid-to-high single-digit progress charges, however not way more.

With this framework in thoughts, let’s now talk about its valuation.

TWLO Inventory Valuation — 12x Ahead non-GAAP Working Earnings

Probably the most constructive facet of Twilio’s funding thesis is that it carries about $1.3 web money. That is clearly a constructive consideration since this quantities to just about 15% of its market cap being made up of money. As an Inflection investor, that is one thing I contend is noteworthy and supportive of the bullish argument.

That being stated, let’s make an estimate of Twilio’s 2025 non-GAAP working earnings.

If we take the excessive finish of Twilio’s guided $675 million of non-GAAP working earnings, and assume that in 2025, Twilio’s non-GAAP working earnings improves to roughly $780 million or a 15% y/y enhance relative to this yr’s non-GAAP working earnings, this leaves Twilio priced at 12x subsequent yr’s non-GAAP working earnings.

On the one hand, I do not imagine many traders would name this an exuberant valuation. And but, a tech enterprise is both disrupting and taking market share or is slowly fading away.

To retain high expertise, executives sometimes meander in direction of profitable corporations, the place their stock-based compensation goes to accrete in worth over time. And I am not satisfied that high executives are going to flock in direction of a enterprise that’s delivering round double-digit progress charges.

Altogether, I am very a lot on the fence with Twilio.

The Backside Line

Paying 12x subsequent yr’s non-GAAP working earnings for Twilio looks as if an inexpensive valuation given the present market surroundings.

Nevertheless, the corporate’s progress prospects have cooled off considerably, with income progress slowing to the only digits and growing competitors. Whereas Twilio’s money place is powerful, making up a considerable portion of its market cap, the macroeconomic challenges and aggressive panorama make it much less enticing for high-growth returns.

At this value level, I imagine Twilio Inc. inventory is pretty valued, and there are possible higher alternatives elsewhere with extra promising progress trajectories.

")

, plus extra! {In the present day Solely}")

soars on cope with Brookfield to energy AI information facilities")

")