")

Profitable of hand dealer buying and selling inventory alternate graph cash, international financial, dealer investor,graph cash of block chain inventory market cryptocurrency promoting and purchase with value chart information graph istock photograph for BL

| Photograph Credit score:

Thitima Uthaiburom

The week earlier than final, US 10-year bonds witnessed the worst week since 2001, with yields spiking 50 foundation factors over the week to 4.5 per cent. Although yields cooled over the week passed by, a brand new drama surfaced with a brewing feud between President Trump and Fed Chair Powell.

Whereas the Trump administration is set to deliver yields on long-term bonds down, the Fed’s choice to attend and watch given tariff-led upside dangers to inflation is enjoying a brick wall. Final week, Trump stated he couldn’t wait to have Powell’s workplace terminated, whereas on the similar time Powell’s chairmanship is legally well-guarded. The impasse is a basic case of when an unstoppable pressure meets an immovable object.

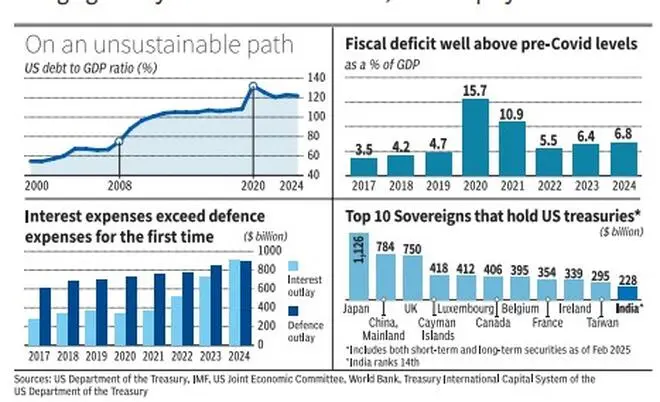

The ‘elephant within the room’ right here is the US authorities’s huge debt pile of $36.2 trillion. The nation has been on a spending spree because the international monetary disaster, which accelerated when the Covid pandemic hit.

Immediately, the US’ debt to GDP stands at a major 122 per cent (December 2024). Bond yields taking pictures up can burn a gap by means of the Federal Authorities’s funds, thus explaining Trump and his administration’s fixation on bond yields. In reality, it was the bond tantrum from the sooner week that pushed Trump to swiftly go gradual on reciprocal tariffs.

Three components

The debt-related issues for Trump administration stem from three components.

First is the refinancing drawback. The earlier administration ducked the rate of interest stress by issuing short-term payments as a substitute of long-term bonds. Whereas the strategy was unsustainable for lengthy, it’s the present administration’s drawback to now refinance them with long-term bonds and can add additional stress on yields.

Two, is the problem of the US authorities’s dependancy to spending, which after all Trump is making an attempt to deal with with DOGE. Whereas the US fiscal deficit cooled to five.5 per cent of GDP in 2022 (calendar yr) after having skyrocketed to fifteen.7 per cent of GDP in 2020 resulting from Covid stimulus, the ratio has now inched again to six.8 per cent. Even worse, curiosity outlay of the Federal Authorities for 2024 surpassed the nationwide defence outlay for the primary time within the nation’s historical past. This reminds of Ferguson’s legislation – ‘any nice energy that spends extra on debt servicing than on defence, dangers ceasing to be a terrific energy’.

The third issue is one that’s self-inflicted. The coverage of the Trump administration, going forwards and backwards, makes an attempt to upend international provide chains and will tarnish the safe-haven standing of US Treasury securities and the worldwide reserve foreign money standing of the greenback. That is the place commerce conflict blows up into capital wars. Though there isn’t a sturdy different to the US greenback but, international central banks may flip to different currencies or gold much more. Per week in the past, speculations have been rife within the bond market that China might retaliate by dumping its holdings of US bonds. This was one of many key causes for the yield to go up the week earlier than final, though the precise purpose for the tantrum remains to be being investigated.

US debt, an fairness woe

Many years earlier, Richard Nixon’s Treasury Secretary famously stated: “the greenback is our foreign money, but it surely’s your drawback”.

Equally, this debt pile of the US and excessive yields are usually not solely an issue for the US, however one for fairness traders throughout the globe. First, the insurance policies that the Trump administration is making an attempt to implement might end in a stagflation within the US, a interval of recession pushed by inflated costs.

High funding bankers have forecast a 50 per cent/60 per cent likelihood of a recession. In a globalised financial setting, this implies a slowdown in international GDP. This mixed with excessive US bond yields, used as benchmark to cost danger property throughout the globe, generally is a double whammy for fairness traders.

Buyers the world over, together with in India, should regulate the US bond market.

Revealed on April 19, 2025