solely $5.68 shipped (Over 16K 5 Star Opinions!)")

")

Run Time: 1H 54M")

")

")

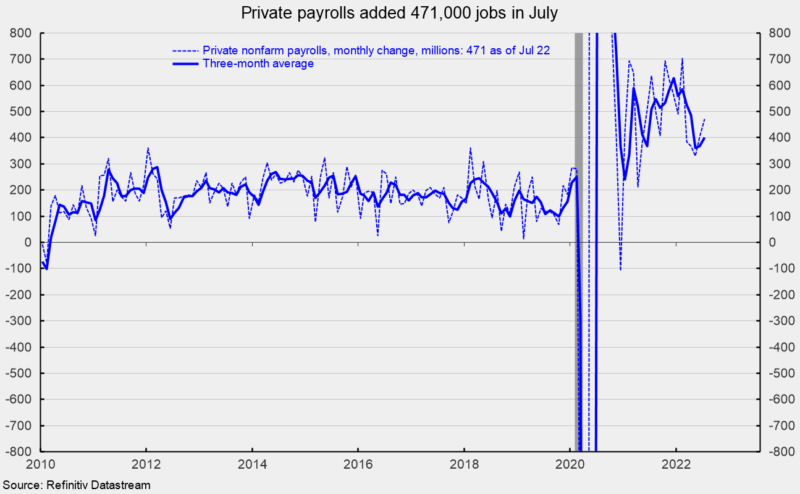

U.S. nonfarm payrolls added 528,000 jobs in July, properly above the consensus expectation of 250,000, and the largest acquire since February. Non-public payrolls posted a 471,000 acquire in July versus consensus expectations of 230,000 and in addition the largest acquire since February (see first chart). General, the roles report is a optimistic consequence.

Regardless of the sturdy outcomes, a considerable preponderance of current information counsel headwinds for the economic system. An aggressive Fed tightening cycle, near-record-low client attitudes, rising preliminary claims for unemployment insurance coverage, and a weakening housing market offset a number of the optimistic results of the sturdy July jobs report. Moreover, ongoing disruptions to world provide chains add to the headwinds. Warning remains to be warranted.

Good points in current months proceed to be broad-based. Inside the 471,000 acquire in personal payrolls, personal providers added 402,000 versus a 12-month common of 424,200 whereas goods-producing industries added 69,000 versus a 12-month common of 71,100.

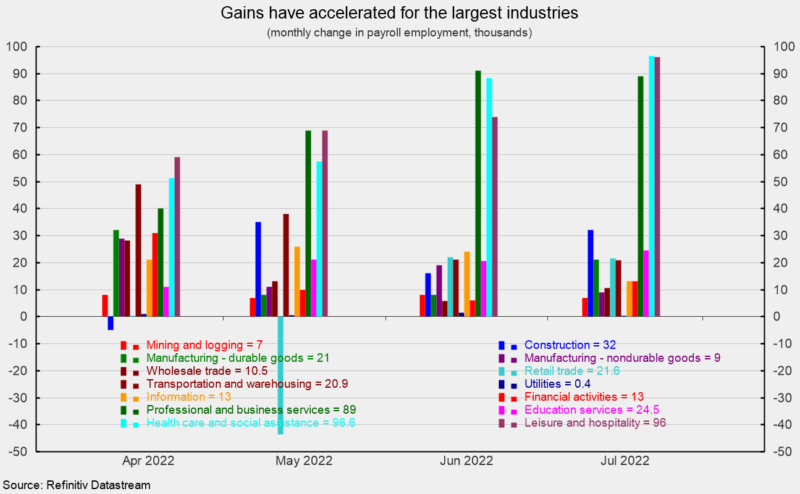

Inside personal service-producing industries, training and well being providers elevated by 122,000 (versus a 66,300 twelve-month common), leisure and hospitality added 96,000 (versus 126,500), enterprise {and professional} providers added 89,000 (versus 96,100), retail employment rose by 21,600 (versus 33,900), transportation and warehousing added 20,900 jobs (versus a mean 36,500), data providers gained 13,000 (versus 16,100), and wholesale commerce gained 10,500 (versus 14,900;see second chart).

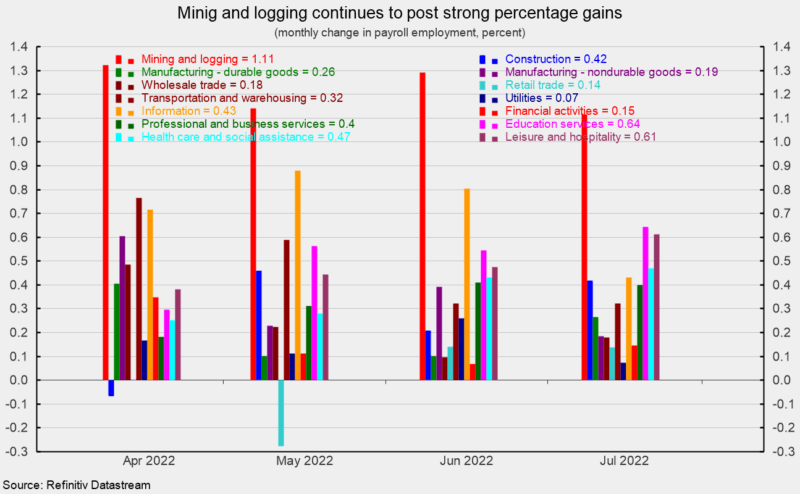

Inside the 69,000 acquire in goods-producing industries, development added 32,000, durable-goods manufacturing elevated by 21,000, nondurable-goods manufacturing added 9,000, and mining and logging industries elevated by 7,000 (see second chart). Whereas precise month-to-month personal payroll positive aspects are dominated by just a few of the providers industries, month-to-month p.c modifications paint a barely totally different image. Mining and logging industries have lately posted sturdy month-to-month share positive aspects (see third chart).

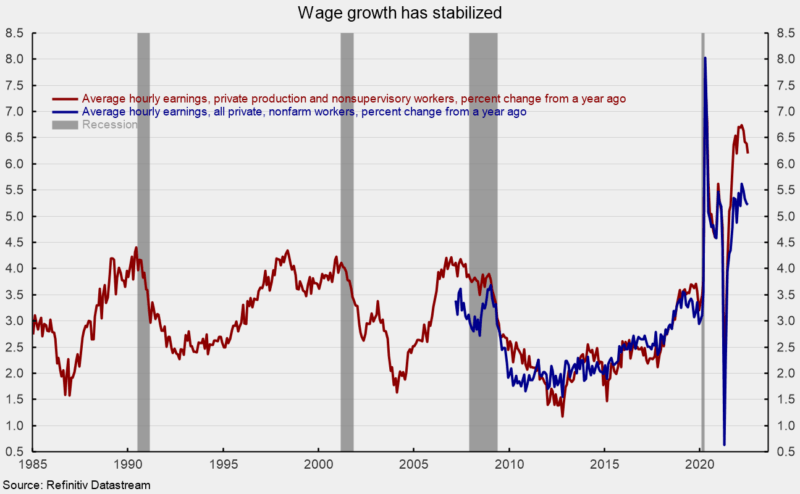

Common hourly earnings for all personal staff rose 0.5 p.c in July, placing the 12-month acquire at 5.2 p.c, about regular since October 2021 (see fourth chart). The typical hourly earnings for personal, manufacturing and nonsupervisory staff rose 0.4 p.c for the month and are up 6.2 p.c from a 12 months in the past, additionally about consistent with outcomes over the past ten months (see fourth chart). The typical workweek for all staff was unchanged at 34.6 hours in July whereas the typical workweek for manufacturing and nonsupervisory held at 34.0 hours.

Combining payrolls with hourly earnings and hours labored, the index of mixture weekly payrolls for all staff gained 0.9 p.c in July and is up 9.7 p.c from a 12 months in the past; the index for manufacturing and nonsupervisory staff rose 0.8 p.c and is 10.3 p.c above the 12 months in the past stage. The full variety of formally unemployed was 5.670 million in July, a drop of 242,000. The unemployment price fell to three.5 p.c from 3.6 p.c in June whereas the underemployed price, known as the U-6 price, remained unchanged at 6.7 p.c in July.

The employment-to-population ratio, one among AIER’s Roughly Coincident indicators, got here in at 60.0 p.c for July, up 0.1 share factors however nonetheless considerably under the 61.2 p.c in February 2020.

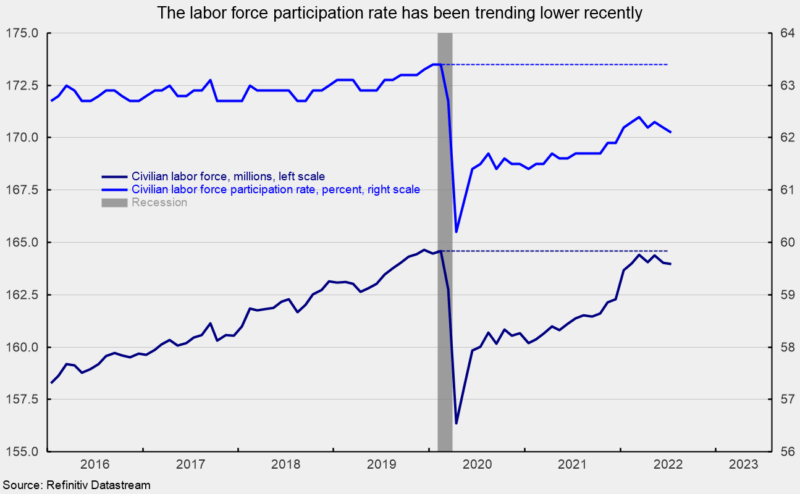

The labor power participation price ticked down once more, falling 0.1 share level in July, to 62.1 p.c. This essential measure has been trending decrease in current months after hitting a pandemic excessive of 62.4 in March 2022 and remains to be properly under the 63.4 p.c of February 2020 (see fifth chart).

The full labor power got here in at 164.0 million, down 63,000 from the prior month and 623,000 under the February 2020 stage of 164.6 million (see fifth chart). If the 63.4 p.c participation price have been utilized to the present inhabitants, an extra 3.4 million staff could be out there.

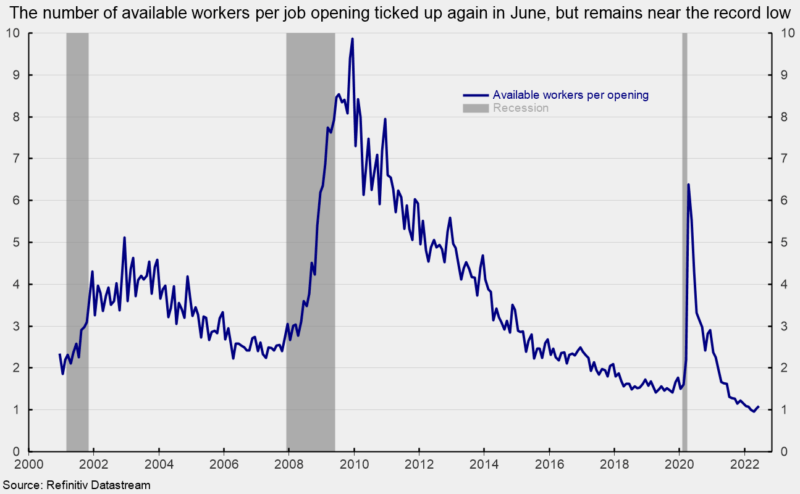

The weaker participation price is one purpose the labor market stays so tight. Primarily based on the most recent Job Openings and Labor Turnover Survey (JOLTS), there may be 1.092 out there staff for every opening, up simply barely from the document low of 0.957 in April (see sixth chart). The most recent Job Openings and Labor Turnover Survey from the Bureau of Labor Statistics exhibits the entire variety of job openings within the economic system decreased to 10.698 million in June, down from 11.303 million in Might; openings have been a record-high 11.855 million in March.

The variety of open positions within the personal sector decreased to 9.766 million in June, down from 10.275 million in Might and a record-high 10.812 million in March. June was additionally the primary month under 10 million since November 2021 and the bottom stage since September 2021.

The July jobs report exhibits whole nonfarm and personal payrolls posted surprisingly sturdy positive aspects. Nevertheless, the upward development in weekly preliminary claims for unemployment insurance coverage and continued decline within the variety of job openings and quits in June counsel offset a number of the optimistic results of the July jobs report.

Persistently elevated charges of rising costs are weighing on client attitudes and could also be beginning to affect spending patterns as properly. Moreover, an intensifying cycle of Fed coverage tightening is rising borrowing prices for customers and companies alike. On the identical time, fallout from the Russian invasion of Ukraine continues to disrupt world provide chains. The outlook stays extremely unsure, and warning is warranted.

Robert Hughes

Robert Hughes joined AIER in 2013 following greater than 25 years in financial and monetary markets analysis on Wall Avenue. Bob was previously the top of International Fairness Technique for Brown Brothers Harriman, the place he developed fairness funding technique combining top-down macro evaluation with bottom-up fundamentals.

Previous to BBH, Bob was a Senior Fairness Strategist for State Avenue International Markets, Senior Financial Strategist with Prudential Fairness Group and Senior Economist and Monetary Markets Analyst for Citicorp Funding Companies. Bob has a MA in economics from Fordham College and a BS in enterprise from Lehigh College.