")

Q3 2025 outcomes")

")

")

bjdlzx

Investment Rundown

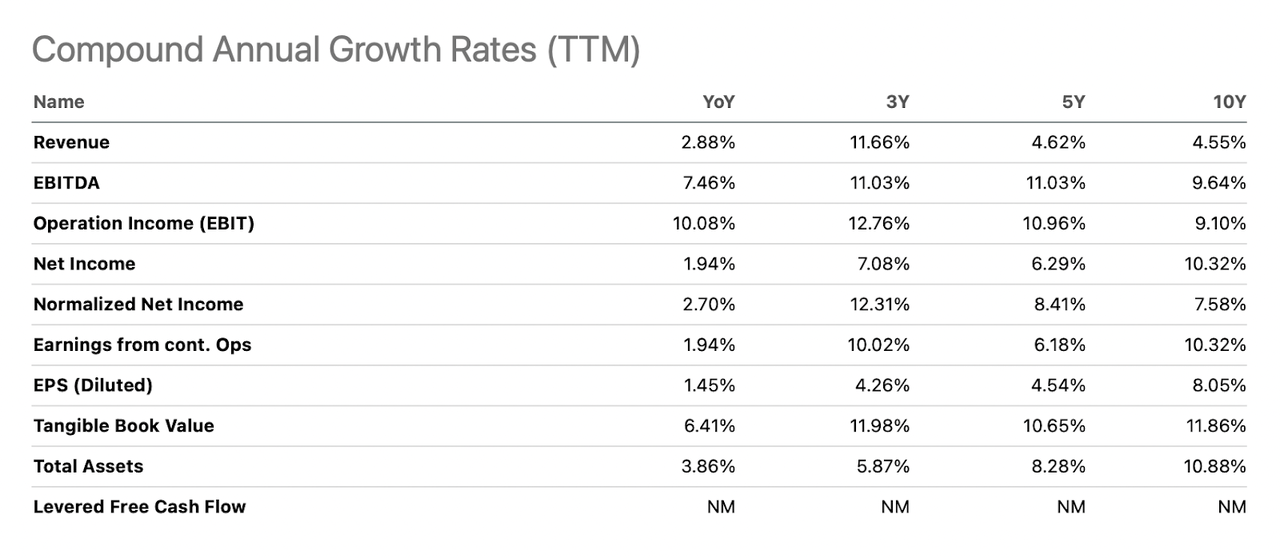

I still think there is a lot of value in investing in the energy sector, even if it has underperformed the broader markets in the last few quarters. The rising oil prices and natural gas prices have been key contributing factors for a lot of growing revenues, certainly the case for Chesapeake Utilities Corporation (NYSE:CPK). The company has averaged an 11.66% compounded revenue rate in the last 3 years alone, a good depiction of the impacts the ongoing war in Ukraine has had on the global energy markets. With this increased level of revenues, CPK has done a decent job in raising its bottom line too, and one of the biggest moves in the company’s history happened last year in September when they announced the purchase of Florida City Gas from NextEra Energy (NEE). This move doubles their presence in the state and should be a good tailwind for increased revenues in the next several years. My issue with the company and why I won’t be rating it a buy comes down to lacking liquid assets and the rich valuation the company exhibits in my opinion.

Company Segments

CPK is an energy delivery company with two primary divisions: Regulated Energy and Unregulated Energy. In the Regulated Energy segment, the company focuses on natural gas distribution in Delaware, Maryland’s eastern shore, and Florida. It also manages regulated natural gas transmission in the Delmarva Peninsula, Ohio, and Florida, alongside regulated electric distribution in Florida’s northeast and northwest regions.

Company Plan (Investor Presentation)

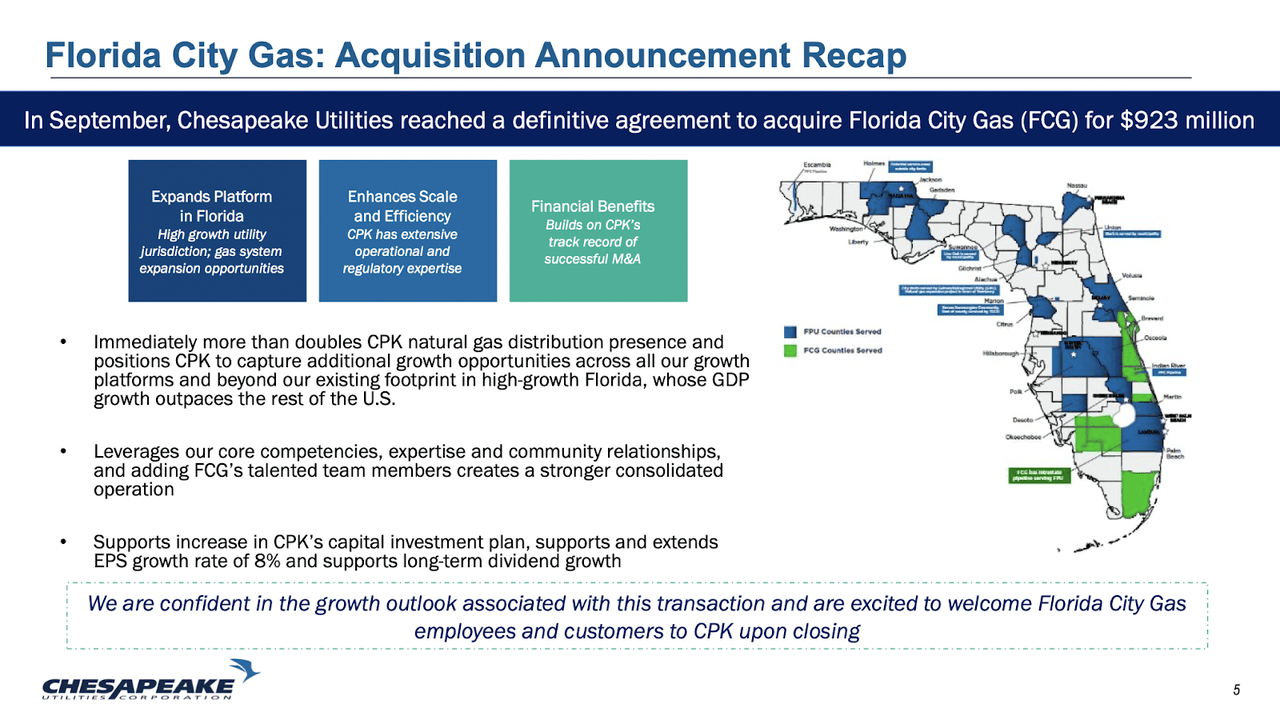

The part of operations in Florida is relatively new, as the company has acquired a large company operating in the region by the name of Florida City Gas for $923 million in total. CPK has had a presence in the state before, but this acquisition more than doubles its presence. The news came out in late September of last year, and it seems the market has not been that keen on the news, seeing as the stock has fallen a fair bit since then. The acquisition has since been completed meaning that in Q4 we should see a slight impact of this, but my eyes are more on the Q1 FY2024 report instead, likely released in April or May. The energy sector as a whole has been facing quite a lot of trouble in the last few quarters, as oil for example has fallen a large amount from its highs in the fall of 2023.

Natural Gas (Trading Economics)

The same has been the case for natural gas too, which CPK is more exposed to and more relevant to the conversation here. Prices of natural gas peaked in the last 12 months in November of 2023, it did rebound, but it’s still down around 30% from the highs.

The Florida Expansions

CPK acquired Florida City Gas from NextEra Energy (NEE) for $923M, including debt, and this was finalized in December meaning that we should see a slight impact of the acquisition in the coming report, but more importantly in the Q1 FY2024 report instead. This acquisition, vital to CPK expansion in Florida, will add 120K natural gas customers and significantly extend its network with 3,800 miles of distribution and 80 miles of transmission lines.

Growth Drivers (Investor Presentation)

The deal will increase CPK’s regulated customer base and net plant by 50% and 30%, respectively, making Florida operations a major contributor to its income and capital plans. CPK has revised its capital expenditure to $1.5B-$1.8B through 2028, with expected earnings of $7.75-$8.00 per share, reflecting an 8% annual EPS growth from the 2025 forecast. Even not that long after the finalization of the deal with Florida City Gas, CPK also acquired J.T. Lee and Son’s which nets them another 3000 customers and 800 000 gallons of propane distributions annually.

Company Growth (Seeking Alpha)

Growth over the years for CPK has been very solid, and the management has proven itself very capable of moving the business forward over the long term. The deal in itself makes sense, as Florida has been one of the fastest-growing states in the country, which rapidly expanded the possible customer base for CPK and other gas companies in the state. This I think further supports a deal like this, which has to be said is very large for a company like CPK, which only has a market cap of $2.2 billion right now. Buying another company for nearly half its market cap will put leverage on the balance sheet and possibly be a reason for the stock price to perform badly in the short term until the actual results of the acquisition are properly displayed on earnings reports. This goes in line with why I think CPK is better off as a hold now, I want to see the results of the purchase rather than almost blindly buying into it. I admit CPK has a strong history of moves like this, but for my risk profile, I rather be a bit late to the party here, rather than too early, and see my position possibly lose a lot in value.

Earnings Highlights

Quarterly Results (Investor Presentation)

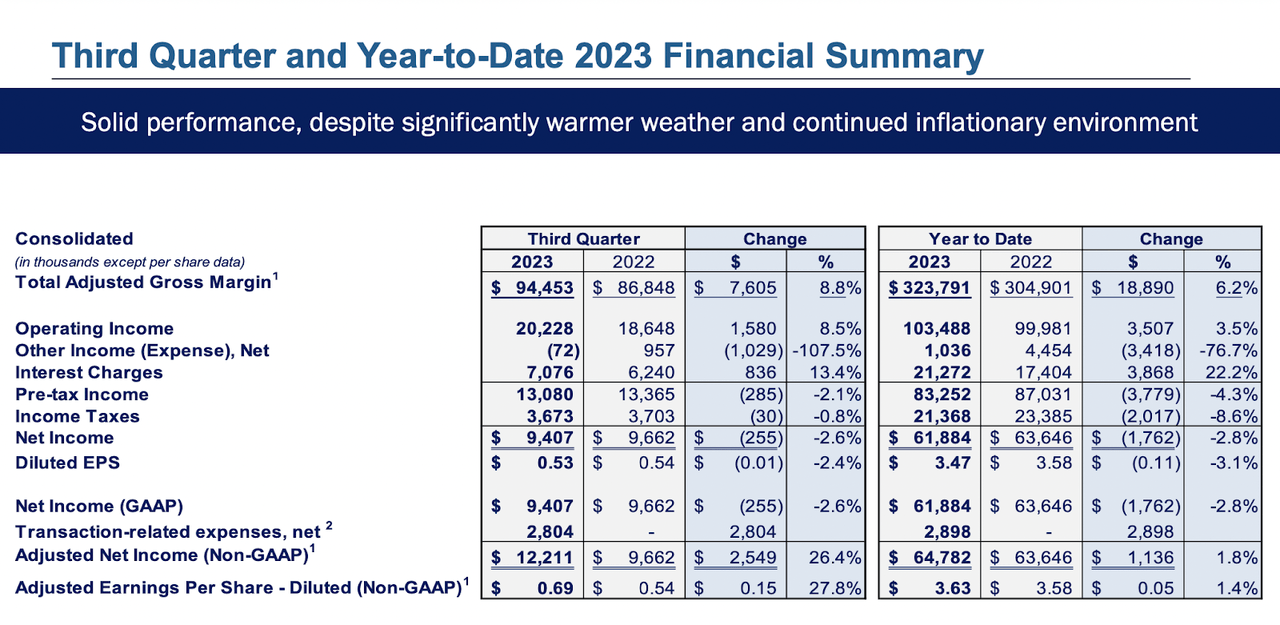

Let’s dive a little deeper into the latest earnings report by CPK, which was released on November 2. It seems we are getting the next earnings report by the company in late February, which gives us room to not make any sudden decisions about whether to buy or hold the stock here. I said previously that this earnings report will be important to see the impact of Florida expansions, as around 1 month should be included seeing as the deal was finalized in early December. But, most of my attention will instead be on the Q1 FY2024 report, which will more clearly show the impact. I do think the EPS will grow on a QoQ basis in the Q1 report as natural gas prices seem to be trending up, and for the coming Q4 report, I think that trend will be visible. Natural gas was volatile in Q4, but ultimately ended higher than the previous quarter.

As far as the numbers go for Q3, CPK raked in $94 million in gross profits and $20 million in operating income, which represented an 8.5% YoY growth rate. CPK does hold a substantial amount of debt and with higher rates, the interest expenses have risen YoY to $7 million now. This ultimately led to the net income declining by 2.6% YoY, but when finalized the incomes to translation-related expenses netted CPK an additional $2.8 million, or $0.69 EPS, a 27.8% YoY increase.

Valuation (Seeking Alpha)

One of the reasons I won’t be rating CPK a buy right now comes down to the lack of appeal of the valuation. With a nearly 45% p/FCF premium to the sector, I don’t think the value can be found right now. The company is making moves to hopefully increase its FCF generation, through the acquisition in Florida, but until it’s seen in black and white I remain a little concerned here. There is value to be had in holding shares though still, as the yield is at 2.23% right now, and CPK has a 20-year history of raising it as well. The payout ratio is not that high, under 50% which leaves CPK with plenty of capital left to make investments like the recent ones. What also holds me back though is the lack of liquid assets on the balance sheet. With barely any cash and $643 million in debt, I would like to see improvements in this area. Even if the debts are still years out to mature, deleveraging and running a less risky balance sheet is something I look for. This leads to me rating CPK a hold for now.

Risks

CPK is notably impacted by the price volatility of propane and natural gas, which poses a significant risk to its financial stability and earnings reports. Market fluctuations in these commodities, influenced by global supply and demand, geopolitical events, and regulatory changes, can lead to unpredictable revenues. Periods of high fluctuations in prices like we have seen now I think have something to do with the poor stock performance for CPK, but it could also be a sector rotation into more growth-oriented stocks, mostly located in the tech sector.

Another notable risk to a company like CPK is warmer weather. This lowers demand for their products as the need to warm homes and buildings becomes less. In the last report by CPK, it seems the impact here in Q3 was about $9.8 million, which is quite extreme seeing as the company nets around $88 million in TTM earnings. Some seasonality is to be expected, but I think one of the better ways for CPK to counteract this is to expand their operations and grow less organically, and more inorganically through acquisitions instead.

Final Words

The gas and utilities sector has been on my radar for some time now, and I find it very rewarding digging through the companies in this sector. CPK is a well-renowned company that has been growing quite well over the years, and the recent expansion in Florida makes a lot of sense, seeing as they already have operations there and the potential customer base is steadily growing each year. However, I still find the price to not present enough value to get in. The value I instead find in holding shares and potentially adding when the price leaves a near 15% discount based on p/fcf to the sector. With a 20-year history of raising dividends, investors can rest assured in my opinion they are still getting their money’s worth holding shares here.