")

")

Q1 2026 earnings report")

")

…and never were.

It has become conventional wisdom among economists that demographics are Japan’s underlying problem. Demographics are blamed for everything from slow growth to zero interest rates to deflation. But demographics are not and never were Japan’s problem. Japan may represent “the future”, but are we drawing the right lessons?

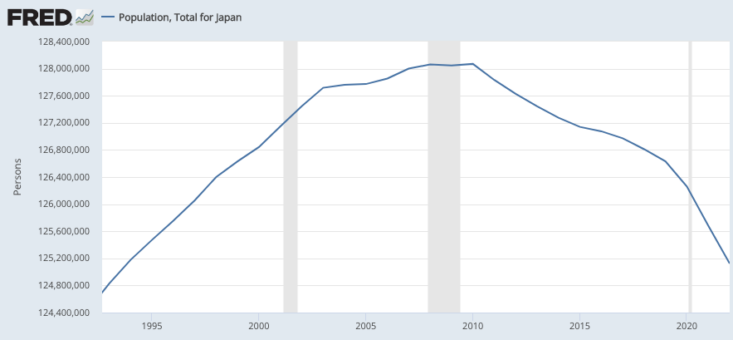

The demographics hypothesis does have a sort of superficial plausibility. Japan’s population grew 12.5% between 1974 and 1991, and then only 3.0% from 1991 to 2012. Japan’s total employment grew 23.6 % between December 1974 and December 1991, and then actually fell by 2.4% over the following 21 years. Thus as population growth slowed, employment growth slowed even more dramatically. At the time, people assumed that an aging population was the culprit.

But when the Abe administration took office at the beginning of 2013, everything changed. Employment soared by 8.1% between December 2012 and November 2019, and yet the demographics actually got far worse.

Population is now actually falling, and at an accelerating rate.

In addition to a falling population, Japan also has an aging population. But that “problem” actually got worse after 2012, so it doesn’t explain the dramatic employment shifts. I use scare quotes, as I’m not convinced that an aging population is actually a problem, at least by conventional metrics. If adults work on average during 75% of their expected adult lifespan, it really shouldn’t matter whether the life expectancy is 80, 180, or 580 years.

Many people (including me a few years ago) assumed that as Japan got older the Japanese would continue to stop working at the same age. But that doesn’t seem to have been the case, and thus the number of available bodies in Japan has risen much more than expected. That reflects both better health and less strenuous jobs.

(In the US, the employment/population ratio for age 55-64 and has hit all time high, while the ratio for over-65 group peaked in late 2019.)

It’s now clear that demographics never were Japan’s problem. Once monetary policy became a bit more expansionary, prices began rising and employment rose much faster than expected. Demographics may partly explain the low real interest rate in Japan, but the nominal rate is mostly determined by the trend rate of inflation, i.e. monetary policy.

In the future, demographics may be a problem for specific countries such as Italy, but only if they choose to make it a problem. There’s no reason to keep the retirement age at 62 as life expectancy rises sharply and jobs get softer. We may choose (in public pension plans) to allow the elderly to enjoy some extra years of retirement as we get richer, but there’s no reason for years spent in retirement to rise one for one with life expectancy. Japan is showing that there’s another way.