")

")

")

")

“Historical past doesn’t repeat, however it usually rhymes,” is a well-known saying attributed to American creator Mark Twain. If you learn at this time’s information concerning the French authorities and its debt state of affairs, it’s not unlikely that the saying involves thoughts.

The European Debt Disaster Revisited

It has been about 15 years for the reason that European Union confronted its first extreme disaster. On account of the aftermath of the Nice Monetary Disaster in 2008, the continent stumbled right into a multi-year debt disaster that introduced huge financial hardship to many members of the Eurozone.

Again then, it was the so-called PIIGS states (Portugal, Eire, Italy, Greece, and Spain) that received into the highlight of monetary markets. After the euro was applied in 2002, these nations had been capable of challenge authorities debt at charges they’d by no means seen earlier than. Unsurprisingly, politicians couldn’t stand up to the strain and issued an increasing number of debt in an try and convey their nations into prosperity.

As all the time, issues that sound too good to be true end up to not be true. And when the urge for food for brand spanking new debt and dangerous credit score abated after the US housing bubble began to burst, it was solely a matter of time earlier than the disaster would unfold and have an effect on European nations that piled up debt underneath the low-interest price regime.

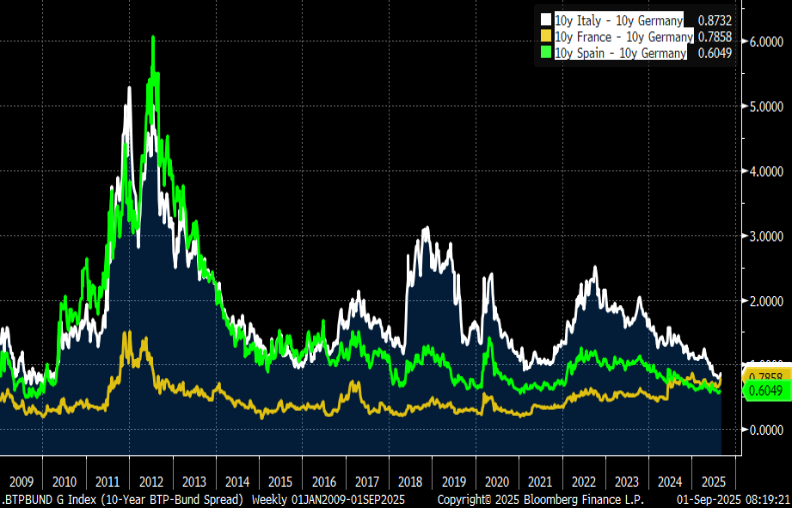

Rate of interest spreads of presidency bonds in comparison with German Bunds (figuratively the “US treasury bond” of the Eurozone) widened considerably. Mario Draghi, then the pinnacle of the ECB, intervened verbally along with his well-known “No matter It Takes” speech, and rate of interest spreads started to slim once more. Greece suffered terribly underneath the disaster. Issues deteriorated to the purpose of requiring monetary help from the EU and the IMF.

The EU additionally put political devices in place, which one way or the other wiggled across the “no-bailout” clause from the Maastricht Treaty. In the long run, one may say that the disaster wasn’t solved, however as a substitute lined up by political actions aimed toward assuaging the nervousness of monetary markets.

Debt Accumulation of the French Authorities

Though France was not essentially a fiscally frugal nation on the time, it didn’t come into the highlight. Notably, France’s rate of interest threat unfold over German Bunds was considerably larger through the peak of the sovereign debt disaster within the 2010s in comparison with its present stage.

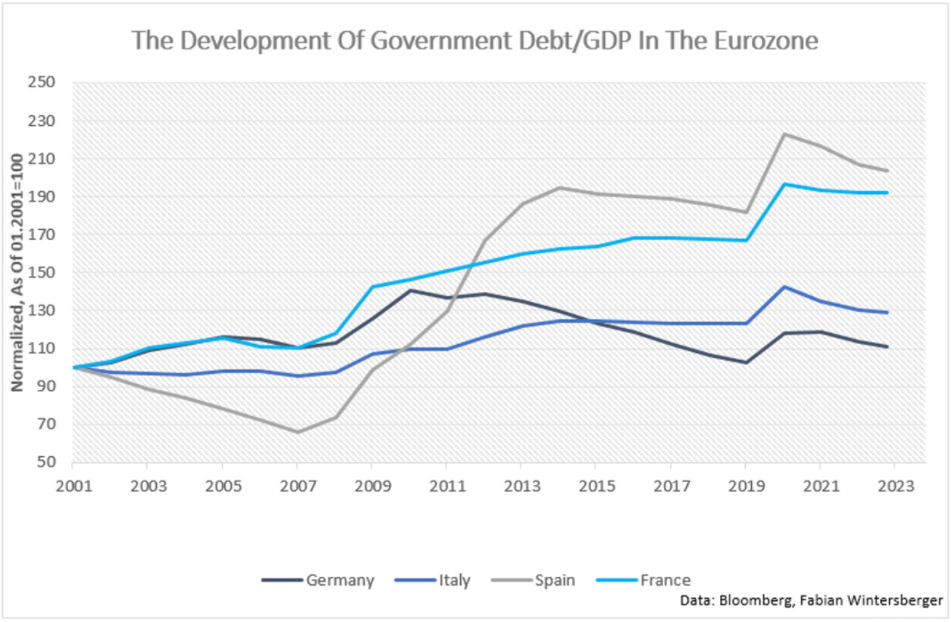

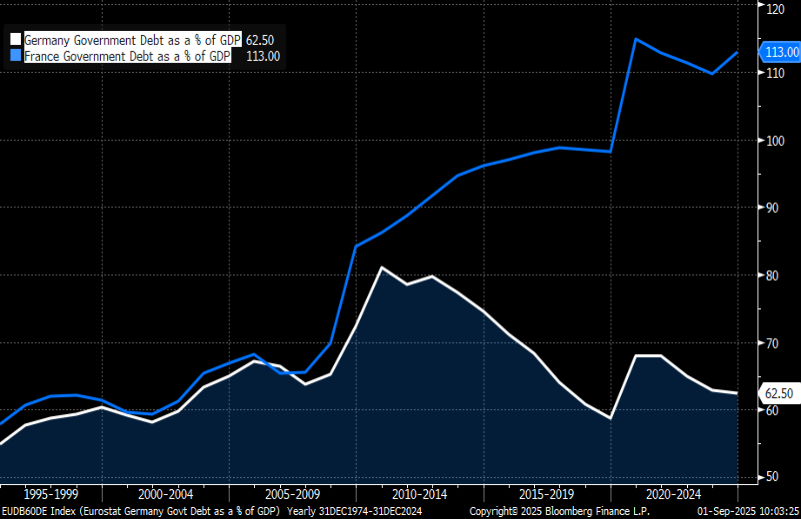

What modified is the debt state of affairs of the French authorities. In 2000, France’s debt-to-GDP ratio stood at roughly 60 %, and it has continued to rise steadily since then. Till 2010, it had climbed to 84 %. On the finish of 2019, it was near 100% and had gone as much as 113 % by the tip of 2024. In proportion phrases, its debt rose a lot sooner than Italy’s.

What’s additionally noteworthy is that the ratio was just like Germany’s till 2008, after which it diverged considerably.

Again within the 2010s, nevertheless, when rates of interest had been falling and close to zero, it was a lot simpler to refinance that debt. The enlargement of the deficit had restricted penalties, as borrowing grew to become cheaper and cheaper.

When rates of interest start to rise, nevertheless, one should borrow more and more more cash simply to pay the curiosity on the debt. In France, the portion of debt-service prices is on its option to turning into the second-largest finances merchandise by 2026, Le Monde reported:

In keeping with authorities forecasts, debt service is anticipated to be the second-largest merchandise of public spending in 2026, with a projected €75 billion. This is able to put it properly forward of nationwide training and protection spending, however behind tax reimbursements to companies and people (linked to tax breaks and different incentive schemes).

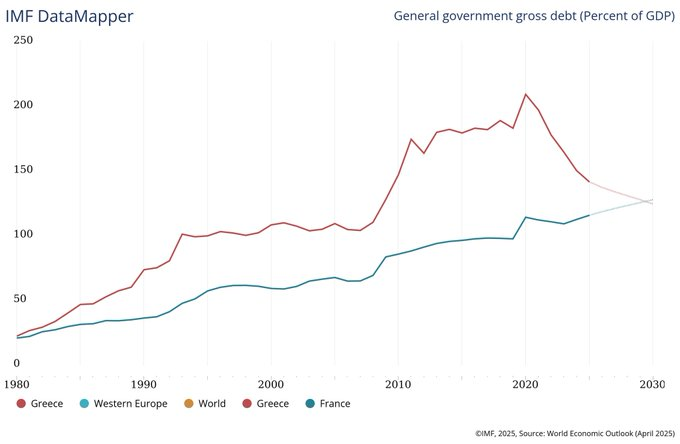

Though the scale of France’s debt remains to be far decrease than in Greece, monetary markets have gotten involved as a result of trajectory of the debt. For instance, whereas Greece has applied fiscal measures and financial reforms to scale back its deficit and has skilled strong financial progress lately, France has seen growing deficits since 2022. At present, the IMF even anticipates that France can have a better debt-to-GDP ratio than Greece.

An Ongoing Political Disaster

Past the darkening fiscal state of affairs, France can also be in a political disaster. In the course of the sovereign debt disaster of the 2010s, France remained a secure political setting. Today are lengthy gone now.

In 2022, Emmanuel Macron secured a victory for the presidency that was nearer than anticipated in opposition to far-right candidate Marine Le Pen. Within the spring of 2024, Macron known as for snap elections, which resulted in a major win for the far-right within the first spherical. Nonetheless, the second spherical ended with a stunning victory of the leftist New-Fashionable-Entrance.

Michel Barnier, a former EU Commissioner, grew to become prime minister in September, solely to lose a confidence vote in December 2024 after he didn’t safe a majority for his Finances. He grew to become the shortest-serving prime minister of France’s Fifth Republic.

The Present Political Disaster

Barnier’s successor, Francois Bayrou, was unable to calm the political turbulence and clear up the finances issues. He invoked particular constitutional powers to cross the 2025 finances and used concessions to the left to outlive a number of confidence votes.

In March, Bayrou proposed extending taxes on the rich and a mechanism that forces people with “extreme financial savings” to put money into protection expenditures. French lecturers rallied behind him and posted an op-ed in Le Monde in help of taxing the “ultra-rich.” But, proof from Norway means that such actions may result in decrease, not larger, tax revenues.

To date, nevertheless, Bayrou hasn’t been capable of safe a majority for the 2026 finances, which additionally goals for drastic spending cuts. Because of this, he determined to take motion: At a press convention on August 25, he known as for a no-confidence vote in Parliament, which he misplaced on September 8.

Calling for the IMF: A Political Maneuver

Because of this, threat spreads on French authorities bonds spiked to their highest stage since January. Finance Minister Eric Lombard warned that snap elections (following Bayrou’s lack of the arrogance vote) may even lead to an IMF bailout. His remark poured extra gasoline on the fireplace.

Nonetheless, the warnings had been clearly a political maneuver to place strain on the members of parliament to help Bayrou on September 8. There’s no arduous proof that France will need assistance from the IMF for the time being, one thing that Christine Lagarde (head of the ECB) confirmed too. Worth motion of presidency bonds after Bayrou’s loss didn’t result in widening threat spreads for French authorities bonds.

France: A Warning To The US

Whereas one can solely speculate, essentially the most possible consequence is a mixture of upper taxes and elevated authorities spending, which then falls in need of expectations and drives the debt-to-GDP ratio larger. Monetary markets will choose the measures as profitable when there’s readability on their effectiveness.

But, Individuals ought to watch the developments in France as a result of it may give an thought of the place the US is headed if it additionally continues to pile up debt. Though President Trump typically promotes low taxes and is pro-business, he has additionally said that he’s open to taxing rich Individuals extra when crucial. Nonetheless, such a state of affairs appears unlikely for the time being. In any case, the US isn’t France, and nonetheless has a considerably decrease debt-to-GDP ratio.

However piling up debt above ranges sometimes seen solely in wartime, in an period the place rates of interest have simply returned to traditionally regular ranges, may additionally result in elevated nervousness in monetary markets sooner or later. If such a case had been to come up, the US may additionally face an identical day of reckoning. Nonetheless, the US additionally advantages from its privilege to challenge the world’s reserve forex. This privilege is unlikely to vanish within the close to future as a result of lack of viable options.