{Right now Solely}")

This autumn 2023 Earnings Name Transcript")

")

Podcast: Play in new window | Download

Whole life insurance can play an important role in your retirement income planning. This statement might go against the grain of advice you see offered by investment salespeople, but I think we’ve displayed ample examples over the past decade that whole life insurance not only works as a retirement income tool, but it accomplishes the task extraordinarily well.

But there’s something else we haven’t spent much time telling you about. Something “baked in” to whole life insurance that puts it in a strong position to deal with rising costs in retirement.

How Do People Generate Income with Whole Life Insurance?

Perhaps you’ve seen a whole life insurance proposal–we often call them “illustrations“–and in this proposal, you saw a static income figure spanning a period like your mid 60’s to your mid 80’s. You might have thought, “hey, that’s cool. I can retire and then receive X amount of dollars every year from this life insurance policy.”

But the truth is people rarely ever do that.

In general, retirees use their assets to generate the income they need–and that’s it.

Whole life insurance is no different in this respect. So while a policy might be capable of producing a certain amount of income, most people tend to use some number less than that.

And taking less money from a whole life policy comes with an added benefit for later in life. Let’s look at an example.

Whole Life Income Example

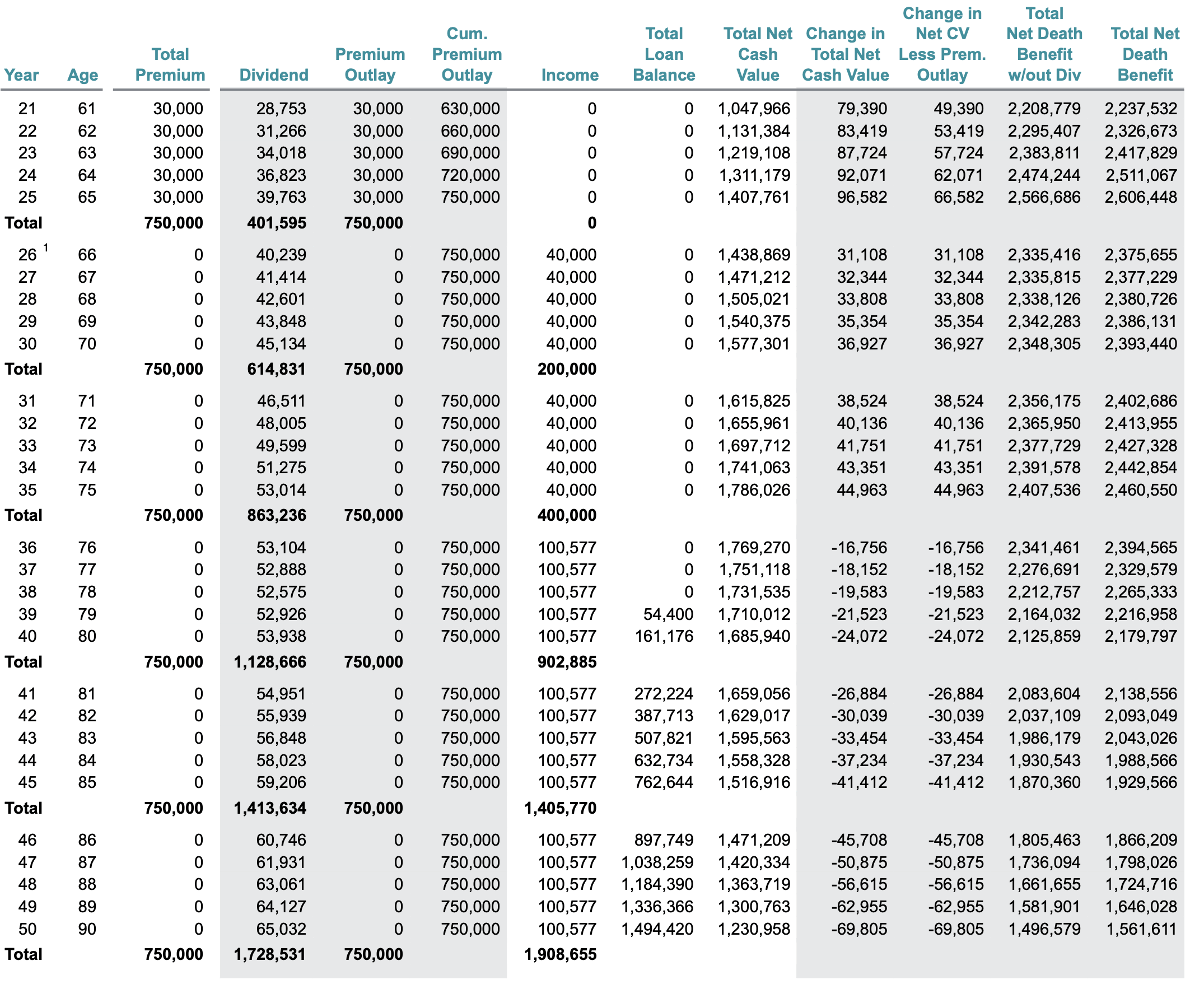

This ledger shows the income results for a 40-year-old male who purchases a whole life policy and contributes $30,000 per year to the policy through his age 65. At age 66, he begins using the whole life policy for retirement income. This ledger shows us the maximum income available to him from age 66 to age 100–the ledger above is a snippet from the full ledger.

As you can see, he can produce up to $72,561 per year with his whole life insurance policy, which isn’t bad at all.

But what if this individual doesn’t need $72,561 in income from his whole life insurance policy. What if he only needs $40,000 per year when retirement begins?

Here’s what that looks like:

Here we see if he uses his whole life insurance policy to cover $40,000 in income needs, he could increase the income to $100,577 per year after the first 10 years of his retirement. This higher income is sustainable–at current dividends–to his age 100.

Using this approach, at age 100, he’d produce about 15% more income from his policy versus taking the maximum amount–$72,561 per year–beginning at retirement and through his age 100. That difference in dollars is about $375,000.

Whole Life Insurance Income is Guaranteed to Get Better

Some of the more savvy readers will likely think to themselves that there is no magic here. After all, if I have $1.4 million in stocks and bonds and if I withdraw a low relative amount against that balance as retirement income I can do the same thing–increase my income later. To this, I would say, yes…theoretically.

You see stocks and bonds might produce a similar result. If we model something using a static rate of return for a hypothetical stock/bond portfolio that exercise will certainly tell us this phenomenon exists with that retirement plan as well. But the difference–it’s subtle but very important–is that stocks and bonds are not designed to do the same thing whole life insurance is.

Whole life insurance will improve over time. It’s contractually guaranteed to do that. Every year you achieve a non-guaranteed result with a whole life contract, the resulting guaranteed components enhance for all years moving forward. So taking less income now with the promise of a higher income capacity in the future is exactly how whole life insurance works.

Stocks and bonds on the other hand only accomplish this task if the rate of return remains positive. This scenario playing out with stocks and bonds is also dependent on the timing of returns–perhaps we should call them, the sequence of returns–on the investment. You might have set out in retirement taking an income that no one would deem dangerously high. You might also experience a market correction that brings your account balance uncomfortably close to requiring a revision to your safe withdrawal rate–perhaps something people are dealing with these days–and this will not permit a larger withdrawal rate after years of lesser income.

But whole life insurance is different. There is no “correction” event with whole life insurance. When markets retract, whole life insurance marches forward, mostly unaffected in the interim. Now, large economic forces can ultimately influence the overall direction of the whole life insurance dividend. We witnessed this playout from roughly 2009 through the modern day. Continuous monetary “easing” from the Federal Reserve brought interest rates to a new level, which ultimately impacted the dividend payments on whole life insurance. But that took a long time to materialize–and most dividend-paying whole life policies continue to compete favorably with similar risk-profile savings plans.

That being said, it’s foolish to overlook the unimpeded progress whole life insurance contracts are designed to have. Taking less income today from your whole life policy does not sacrifice the maximum you have available to you. Even if the dividend declines, the guaranteed features of the contract are the primary drivers of this attribute.