(ERIC) Q4 2025 Earnings Call Transcript")

")

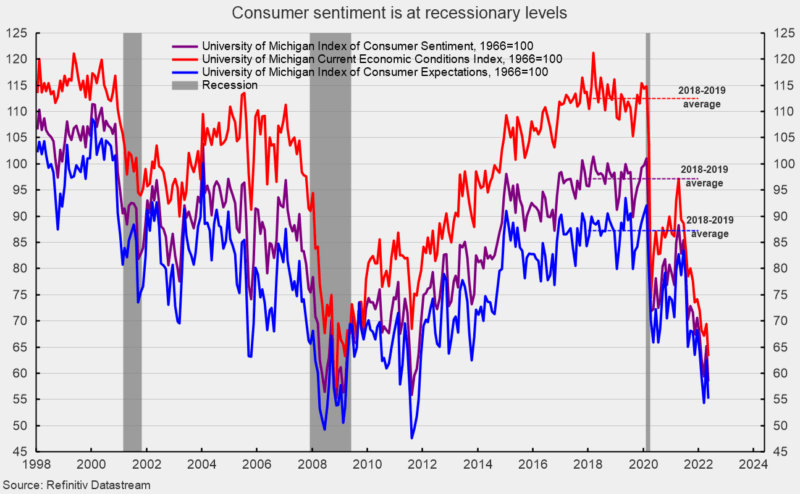

The ultimate Might outcomes from the College of Michigan Surveys of Customers present general shopper sentiment continued to fall within the latter a part of Might. The composite shopper sentiment decreased to 58.4 in Might, down from 59.1 in mid-Might and 65.2 in April. The ultimate Might result’s a drop of 6.8 factors or 10.4 p.c. The index is now down 42.6 factors from the February 2020 end result and on the lowest degree since August 2011 (see first chart).

Each part indexes posted declines. The present-economic-conditions index fell to 63.3 from 69.4 in April (see first chart). That could be a 6.1-point or 10.0 p.c lower for the month and leaves the index with a 51.5-point drop since February 2020 and places the index at its lowest degree since March 2009.

The second sub-index — that of shopper expectations, one of many AIER main indicators — misplaced 7.3 factors or 11.7 p.c for the month, dropping to 55.2 (see first chart). The index is off 36.9 factors since February 2020 and is on the second-lowest degree since November 2011.

All three indexes are close to or beneath the lows seen in 4 of the final six recessions.

In accordance with the report, “This latest drop was largely pushed by continued unfavourable views on present shopping for circumstances for homes and durables, in addition to customers’ future outlook for the economic system, primarily attributable to issues over inflation.” Nevertheless, the report provides, “On the identical time, customers expressed much less pessimism over future prospects for his or her private funds than over future enterprise circumstances. Lower than one quarter of customers anticipated to be worse off financially a yr from now.” Moreover, the report states, “Wanting into the long run, a majority of customers anticipated their monetary scenario to enhance over the following 5 years; this share is actually unchanged throughout 2022. The report’s take-away, “A secure outlook for private funds could at the moment help shopper spending. Nonetheless, persistently unfavourable views of the economic system could come to dominate private elements in influencing shopper conduct sooner or later.”

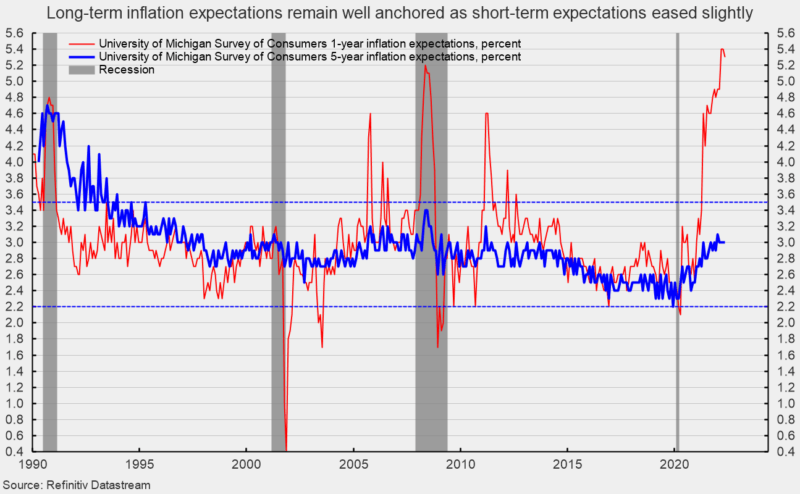

The one-year inflation expectations ticked down barely to five.3 p.c in Might, down from 5.4 p.c in April. The one-year expectations has spiked above 3.5 p.c a number of instances since 2005 solely to fall again (see second chart). The five-year inflation expectations remained unchanged at 3.0 p.c in Might. That end result stays effectively inside the 25-year vary of two.2 p.c to three.5 p.c (see second chart).

The weakening pattern in shopper attitudes displays a confluence of occasions with inflation main the pack. Persistent elevated value will increase have an effect on shopper and enterprise decision-making and warp financial exercise. General, financial dangers stay elevated as a result of affect of inflation, the beginning of a Fed tightening cycle, the Russian invasion of Ukraine, and renewed lockdowns in China. The ramping of unfavourable political advertisements because the midterm elections method may additionally weigh on shopper sentiment in coming months. The general financial outlook stays extremely unsure.

Robert Hughes

Robert Hughes joined AIER in 2013 following greater than 25 years in financial and monetary markets analysis on Wall Road. Bob was previously the top of International Fairness Technique for Brown Brothers Harriman, the place he developed fairness funding technique combining top-down macro evaluation with bottom-up fundamentals.

Previous to BBH, Bob was a Senior Fairness Strategist for State Road International Markets, Senior Financial Strategist with Prudential Fairness Group and Senior Economist and Monetary Markets Analyst for Citicorp Funding Providers. Bob has a MA in economics from Fordham College and a BS in enterprise from Lehigh College.