")

")

Common house costs stay very near the all-time highs reached in the beginning of the yr. Accordingly, public opinion surveys present rising concern concerning the situation of housing affordability, and politicians are taking discover. The Trump administration has waded in with a probably forthcoming nationwide housing emergency declaration so the President can do… one thing. We could have to attend till a decree is issued to see what precisely Mr. Trump thinks his emergency powers are within the realm of housing coverage.

However are homes actually costlier over the long term, or is it simply an financial mirage? As an economist with a background in residential development, I take into consideration this situation typically.

Once I learn articles concerning the housing affordability disaster, I are likely to agree with the economically-informed consensus that America has a basic housing provide drawback. A mix of regulatory constraints—zoning, allowing, energy-efficiency requirements, occupational licensing, and so on.—raises house development prices. Tariffs and the purge of unlawful immigrant labor are usually not serving to, both. I endorse the argument that regulatory easing would make housing considerably extra inexpensive.

However, I sense that a lot of the fuss about ever-rising house costs relies on incomplete evaluation. It doesn’t account for sufficient of the related components to supply a passable clarification of the noticed developments within the knowledge. Good financial evaluation should maintain different components fixed—the well-known ceteris paribus assumption. On the subject of house worth evaluation, there’s a raft of different components to think about. Some pretty easy calculations with simply accessible knowledge help an argument that house costs are usually not considerably greater than their long-run common.

The Different Elements that Matter in Housing

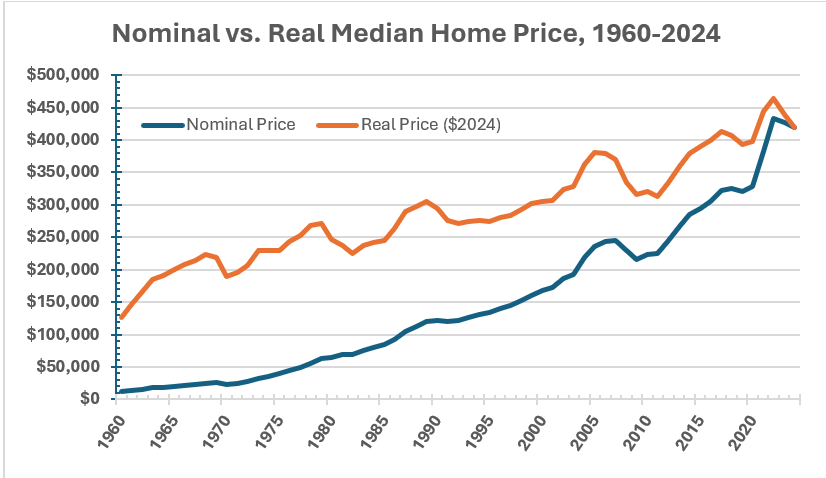

So what are the ceteris we should maintain paribus when analyzing long-run developments in US house costs? Let’s begin with the massive, apparent one: inflation. We are able to’t evaluate nominal house costs from 2019 to 2025 (CPI grew 26% over these six years alone), a lot much less from 1990 or 1960 or no matter date one selects because the golden age of affordability.

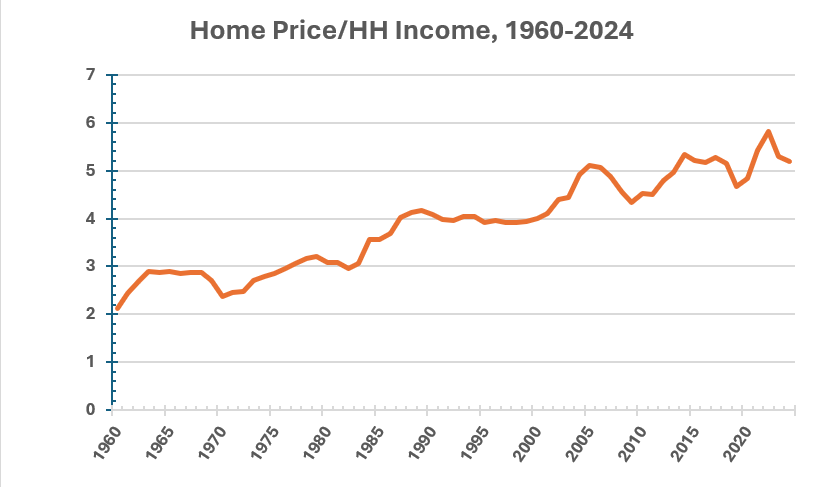

Let 1960 (the earliest yr for which I can acquire knowledge factors for all of my ceteris paribus classes) characterize the paragon of house affordability within the US. Whereas the nominal median house worth rose by 3,421% from 1960 to 2024, adjusting this for inflation utilizing the Shopper Worth Index reveals a extra modest however maybe nonetheless distressing rise of 232%. However let’s now additionally consider a lot smaller, however vital, development in family incomes over this time-frame. The everyday observe is to divide the median house worth by the median family revenue to get the house worth/ family revenue ratio. In actual phrases, this ratio rose from about 2.1 to about 5.2, or 145%, over the identical time-frame.

Subsequent, let’s contemplate what, precisely, individuals are getting with their buy of the median house. In 1960, the median house constructed within the US was 1,500 sq. ft. Median house dimension rose steadily, peaking at about 2,700 sq. ft within the mid-2010s earlier than declining barely to 2,400 sq. ft in 2024. Assuming larger is healthier and that individuals are glad to shell out more cash for extra home, we will alter for this dimension issue by calculating actual house worth per sq. foot of house dimension. This metric elevated by 107% from 1960 to 2024. Nonetheless a big enhance, however much more manageable than that uncooked actual median worth by itself or adjusted merely for family incomes.

We’re getting nearer, however I need this to be a complete adjustment. One crucial analytical issue I realized from the nice Thomas Sowell is to be looking out for composition results, or adjustments within the traits of teams over time that may skew simplistic statistical snapshots. Sowell teaches us to be looking out for composition results in any family statistic, as a result of family dimension can and does change considerably over time. In 1960, the common US family was 3.33 individuals. This determine dropped to about 2.5 by the 2020s, with most of that decline happening earlier than the Nineties.

Which means that the median family revenue is split amongst a smaller variety of family members, understating the expansion of family revenue over time on a private stage. In different phrases, actual median family revenue per individual went up by greater than is obvious within the general family revenue knowledge sequence. We are able to issue this into our house worth evaluation by calculating the ratio of actual house worth to actual family revenue per individual. This metric rose by 96% over the 1960–2024 interval.

Lastly, let’s mix the change in house dimension together with the change in family composition in that final calculation. Our remaining adjustment leads to the ratio of actual house worth per sq. foot to actual family revenue per individual. Drumroll, please: by this comprehensively adjusted metric, housing affordability rose by a paltry 6% from 1960 to 2024, and is definitely down considerably from its peak within the late Seventies.

Furthermore, all of those changes don’t account for maybe crucial change: that of house high quality when it comes to options and facilities which have turn out to be extra frequent over time. I’ve but to seek out an index of house high quality that tracks these attributes in a dependable means. I do have a robust impression, primarily based on private expertise and tidbits of knowledge, from which I arrive at a assured conclusion that as we speak’s houses are nicer locations to dwell than these of 30 or 60 years in the past. As a 2011 US Census report summarizes, along with bigger house sizes, “houses constructed as we speak have virtually extra of all the pieces—several types of rooms reminiscent of extra bedrooms and loos, extra facilities reminiscent of washers and dryers, rubbish disposals and fireplaces, and extra security options, reminiscent of smoke and carbon monoxide detectors and sprinkler methods.” At present’s larger, roomier houses even have extra energy-efficient utilities, extra user-friendly home equipment, extra storage area, larger and extra well-appointed kitchens the place stone counter tops changed Formica, and so forth. If we might discover a technique to consider all of those adjustments to the excellent house worth adjustment, it would present zero change or perhaps a fall in house costs, ceteris paribus.

In conclusion, the housing affordability disaster is a nothingburger!

Whereas it’s vital to consider carefully concerning the adjustments within the ceteris, I wish to reiterate that there’s a housing worth drawback, and it deserves consideration and a sensible public coverage response. I hope my “complete” actual house worth changes listed below are thought-provoking, however this evaluation is missing in at the least two main methods: 1. It cherry picks the beginning and finish factors; 2. It’s nationwide combination knowledge, so it doesn’t decide up regional variations in house worth adjustments over time.

In case you take a look at ten-year spans, there’s a number of fluctuation in house worth shifts, even by my most popular ratio of actual house worth per sq. foot to actual family revenue per individual metric. 2024 costs had been 22% greater than 10 years prior, giving the up-and-coming era ample grounds to complain that house costs are getting out of attain. The latest spurt of house appreciation additionally validates the criticism that housing markets serve to switch wealth from poorer millennials to well-off boomers. Housing worth development additionally varies vastly by area. Scorching markets—largely coastal and sunbelt metros—noticed 10-year worth development at 1.5 to 2 occasions bigger than the nationwide common. Cooler markets in elements of the south and Midwest noticed development charges not a lot greater than general CPI inflation.

As this glorious map from Visible Capitalist reveals, it’s a lot simpler to afford a home (ceteris paribus, in fact!) within the Midwest than within the West, Northeast, or Florida. (I knew there needed to be a compensating differential for our depressing Michigan winters!)

Getting a deal with on escalating house costs is a straightforward, however not politically simple, repair. We have to claw again the relative development in house development prices. In different phrases, we want the housing provide curve to “shift to the precise” greater than the demand curve has shifted. Builders know precisely what this could take: much less restrictive zoning (particularly for multifamily items), simpler licensing and allowing processes, much less stringent constructing codes and vitality requirements, freer markets in labor and supplies, and perhaps a client acceptance of smaller, less complicated houses.

Dataset and calculations accessible upon request: [email protected]

Tyler Watts is a professor of economics at Ferris State College.