")

5 Years In the past, This is How A lot You’d Have As we speak")

")

")

Q2 2025 earnings leap on increased revenues")

")

More than half of Chinese children want to be astronauts when they grow up. That’s not just because the CCP is telling them what to say and how to say it. China is an amazing country where work ethic and family values are reminiscent of the U.S. in the 50s (though they’ve started copying America’s bad habits lately), but that’s not what makes her children gaze longingly into the skies. They weren’t weaned on Star Trek and Star Wars, they’re just expressing the same feelings mankind has evoked since we first walked this planet. This primal fascination extends to the retail investment community as well. After cannabis, space probably attracts more newbie investors than any other theme we cover. Not coincidentally, cannabis and space are the two themes we have the least amount of exposure to.

That’s intentional, because themes that attract newbie investors will be more volatile and easier to manipulate. Look no further than meme stonks for evidence of how much noise retail investors can create. Despite these risks, we need to consider if increasing our exposure to space stocks makes sense given we’re in a bear market and have cash in our tech stock portfolio to deploy. Given that we don’t invest in stocks with a market cap less than $1 billion, many deeply discounted space SPACs aren’t on our radar (company names link to our latest research pieces).

Our recent YouTube video on Starlink Stock: A Trillion Dollar Opportunity talked about how SpaceX is currently the leader in launching things into space, while their subsidiary, Starlink, has deployed the largest satellite constellation known to man. Investing in space companies that are competing with SpaceX or Starlink probably isn’t a good idea.

Geospatial intelligence is a category of stocks that seems impervious to Musk’s attempts at conquering outer space. Planet Labs is the leader in imaging, and the recent planned acquisition of Maxar Technologies (MAXR) by private equity firm Advent bodes well for other depressed names in geospatial imaging, a category of NewSpace that Starlink doesn’t seem likely to dabble in. That’s because the value add comes down to how well the data is interpreted and mined for insights.

Also attractive are companies attempting to move beyond launching rockets or building satellites into offering a variety of pick-and-shovel plays on the space theme. Aside from Planet, just one space SPAC stands out as a company we might possibly like to own.

Rocket Lab’s Revenue Growth

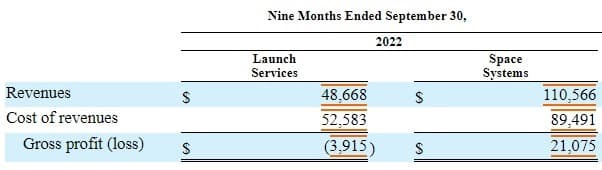

Are you someone with a little rocket icon in your Twitter profile? Well open up that jar of Vaseline and close the window shades. We’re about to say favorable things about your sacred cow, starting with showering praise on the company’s ability to absolutely trounce their revenue estimates. While the glossy SPAC deck promised $176 million for 2022, the company is on track to deliver $210. The problem is, all that revenue costs a lot to produce. Over the past four quarters, the company has managed a blended gross margin of around 13%. Digging into the details shows that launching rockets isn’t a profitable business for Rocket Lab (RKLB).

The “Space Systems” segment would be realizing gross margins of 19% were it not for the losses being incurred by “Launch Services.” Those aren’t SaaS-like margins, but they’re better than the 11% gross margins seen from the combined segments. Perhaps launches aren’t profitable because Rocket Lab hasn’t mastered reusability.

Look, the majority of the cost of the rocket is in the first stage. If you can get that first stage back in a good condition and service it without having to rebuild it completely, then it is a very, very strong performance driver from a margins and cost perspective.

Credit: Rocket Lab Q3-2022 Earnings Call

Our recent video on Starlink incorrectly stated that Rocket Lab was giving up on catching Electron boosters using a helicopter when it appears that’s still a major focus for the company. The first attempt saw the helicopter operator manually drop the booster following a successful catch. The second attempt saw a telemetry problem which involved the orientation of the falling object to the helicopter. There are several videos out there – dramatic music and all – that show the process taking place and it’s all rather manual and seems quite difficult.

We’re not rocket surgeons, we’re MBAs, but will this process work with a booster that’s much bigger? The new generation rocket, Neutron, is expected to benefit from the lessons they’re learning about reusability today. So, will they catch Neutron boosters with a bigger helicopter? With two helicopters? But maybe we’re getting a bit ahead of ourselves. First, the company needs to consistently retrieve boosters from Electron rockets that they’ve already launched 30 times. Given the human error element in utilizing a helicopter to catch a flying object, one wonders what the probability of success will be per 100 launches. That needs to be factored into COGS as well.

Rocket Lab is one of two stocks in our disruptive tech stock catalog that we like. The other is MDA (MDA.TO).

A Good Problem to Have

Being a successful investor is as much about controlling your emotions as it is about picking the right companies to invest in. Being comfortable watching a stock in your portfolio get decimated, and having the cojones not to sell at a loss, is crucial to being a successful disruptive tech investor. It’s about time in the markets, not timing the markets. So, when shares of MDA have fallen 63% since we last wrote about the company (compared to a benchmark fall of 9.5% for the TSX), is there reason to be concerned?

The last time we checked in with MDA stock was a May 2021 piece titled MDA Stock Offers Diversified Exposure to Space Theme. We liked the diversified revenue segments, but didn’t see the revenue growth we expect from disruptive tech stocks. That’s since changed as they’ve shown nice consistent growth across the past four quarters from three revenue segments.

Looking through their Canadian filing documents shows several items of concern. There’s $712 million dollars in intangible assets and goodwill that might result in future impairment charges, especially given the plummeting share price. There’s also $143 million in debt that comes with some covenants. Aside from that, revenues are growing at a decent clip as the company valuation plummets compared to other space stocks in our universe.

Note that Maxar traded at a simple valuation ratio (SVR) of one before they were recently acquired by Advent which boosted the SVR to three on the news. Speculators will point to the propensity of private equity firms to consolidate within sectors, noting that perhaps an acquisition could be in the cards for MDA. We don’t speculate on the possibility of M&A events, and we would never invest in MDA for one key reason.

Having hard rules that you follow with no exceptions makes life much easier in times like this. We don’t invest in companies with a market cap of less than $1 billion. MDA’s market cap is currently $506 million. Buying shares of a company that’s below our market cap cutoff is out of the question. That said, it’s hard to see why we wouldn’t have a good think about going long if that rule wasn’t in place.

As we look to streamline our tech stock report, we’ll be removing MDA and keeping it in our catalog as a like. Hopefully, the company pursues a listing in the United States, something that would increase participation from institutional investors and shore up the valuation.

Conclusion

Space and cannabis are probably the riskiest investment themes we cover and some of the most popular stocks among newbie investors. If you loved Space SPACs before, you must really love them at these bargain basement prices. While MDA stock has fallen off our radar due to size rules, we’re in no hurry to invest in any space stock. It should be pretty clear by now that FOMO has cost investors a lot of money. We’ll continue watching Rocket Lab to see if the reusability problem gets suitably solved before investing in the stock. That should help address their low gross margins as well.

Tech investing is extremely risky. Minimize your risk with our stock research, investment tools, and portfolios, and find out which tech stocks you should avoid. Become a Nanalyze Premium member and find out today!