")

Q2 2026 earnings")

")

")

Hold these 4 issues in thoughts and construct generational wealth

Fascinated about the long run isn’t horny. We like dwelling within the “now.”

There’s no time like the current, particularly for the younger, working grownup.

Properly, the current referred to as, and the buyer value index rose 9.1% since final June. Inflation is having a hall-of-fame season this yr.

How does that make you are feeling in regards to the buying energy of your greenback? I guess you don’t need to work your entire life, so ultimately, you’ll want some cash saved up for retirement.

Listed below are 4 errors to keep away from so that you will be comfy financially sooner or later.

In a Roth IRA, you place post-tax {dollars} into a person retirement account. In contrast to a standard IRA, you’ll be able to withdraw with out paying taxes in your contributions, however not till you’re 59 and a half.

You can also’t withdraw your funds inside 5 years of opening the account, counting from the tax yr of your first contribution or extra. However that does not matter if you happen to begin investing at a younger age.

Consider it like this — taxes suck, proper? So why pay taxes in your investments twice?

How a lot are you going to take a position per yr anyway?

In case you observe the 50–30–20 rule (I’ll discuss extra about this later), the 20 represents the share of your month-to-month earnings you need to save or make investments.

Now, you are able to do rather more along with your financial savings than put money into a ROTH IRA, primarily as a result of there’s a most contribution per yr.

The utmost complete annual contribution for all of your IRAs mixed is $6,000 if you happen to’re underneath 50 and $7,000 if you happen to’re 50 or older.

So think about you make $50,000 earlier than yearly taxes — you need to make investments 20% or $10,000 yearly. You would possibly as effectively put $6,000 right into a ROTH IRA, divvy the cash into just a few index funds, and let your cash compound over time.

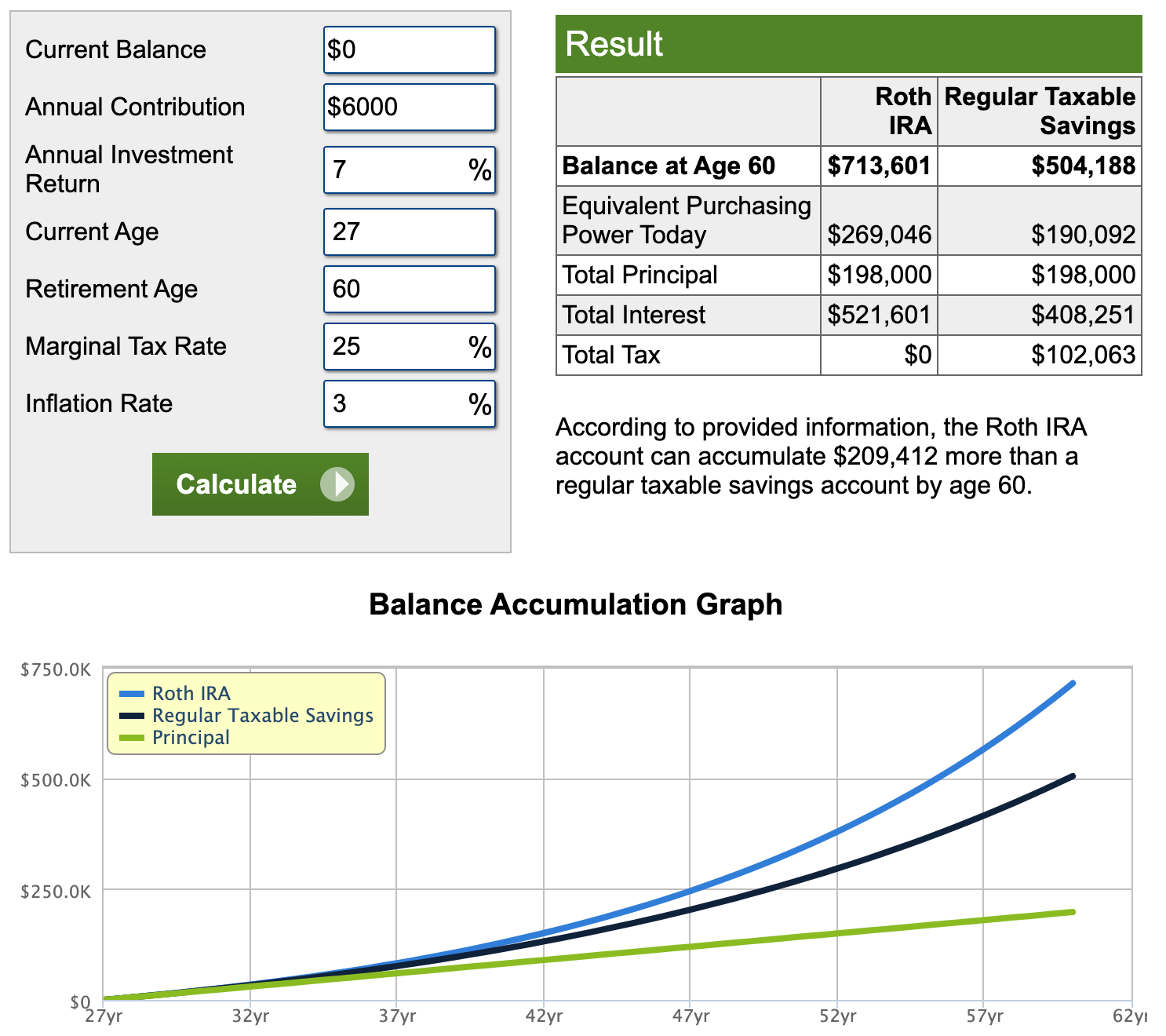

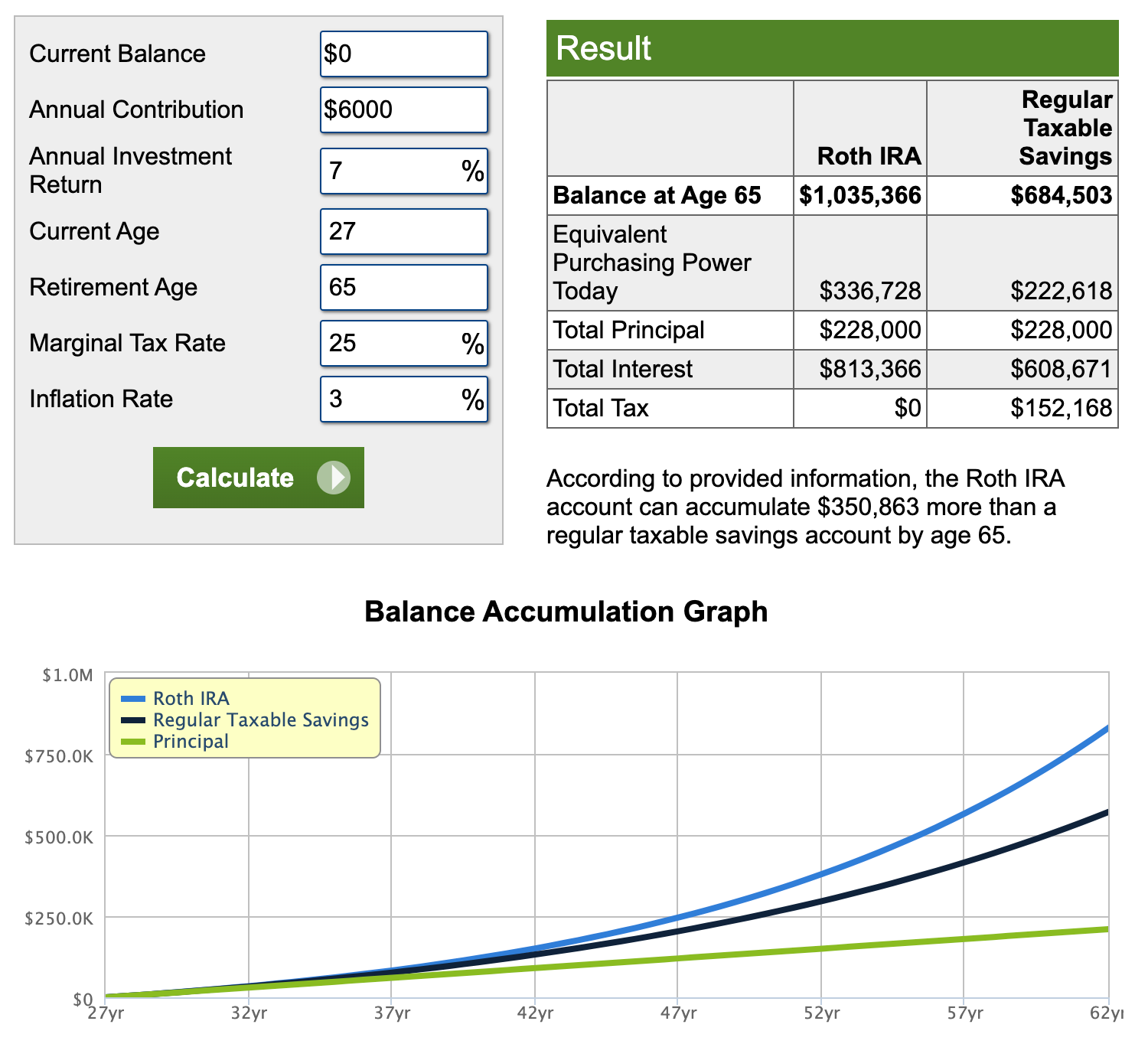

Compounding is a strong pressure. Take a look at these two charts for reference.

On the left, if you happen to had been to take a position $6,000 per yr, beginning at 27, assuming 7% annual returns, you’d have $713,601 in your account.

However wait 5 years till you’re 65, and also you’d have over $300,000 extra.

Isn’t that loopy? That’s as a result of the longer you let your cash be just right for you, the extra doubtless you’ll obtain monetary freedom.

And don’t fear, solely nonqualified withdrawals out of your Roth IRA create extraordinary taxable earnings at your marginal tax charge.

My Robinhood account appears to be like like a rollercoaster after plummeting downhill at 60 miles per hour.

On the time of writing, the S&P 500 is down 19.65% year-to-date. Different shares, index funds, and ETFs have largely adopted go well with.

We’re in a bear market, probably heading towards a recession. In case you’ve held onto any small or giant cap shares since 2021, they’ve doubtless plummeted fairly a bit.

Fortunately, I’ve by no means invested cash I don’t want proper now, however I paid the value of tuition. Trying again, I ought to’ve identified what would occur, however how might I?

I began investing in 2020 and acquired caught available in the market’s hype.

Small caps had been rising exponentially, tech was booming, and other people thought Ethereum would hit $10,000. However when the market began to take a flip for the more severe, I made one of the best resolution I probably might have.

I didn’t promote out of worry.

Investing is all about psychology. Shopping for particular person shares, even small caps isn’t an issue. The issue is while you by accident switch your wealth to those that know what they’re doing.

An important lesson is to reverse what you suppose is appropriate for the market. If the market is rising at a historic charge, it’s not a very good time to get in.

Warren Buffett famously stated:

“Be grasping when others are fearful, be fearful when others are grasping.”

For the millennials and Gen Z’s, right here’s a meme that’ll make extra sense.

After I began investing, I didn’t understand the federal government printed greater than $3 trillion in 2020 alone (virtually 20 % of all current USD).

Then we acquired our stimulus checks. We had extra free time than ever however nowhere to spend the cash due to the lockdowns. So we opened up Robinhood accounts and began buying and selling.

The retailer investor acquired consideration, and we had been enthusiastic about Gamestop, however this inflow of cash into the markets got here at a value. All that printed cash exponentially inflated the financial system, and at the moment, the truth of inflation scared us.

We began pulling cash out of shares in troves, and the market tanked by greater than 20% this yr.

The lesson: You may put money into particular person markets however select to put money into firms you genuinely consider will thrive over the subsequent 20 years. Don’t promote; simply strengthen your positions.

Except you’re a full-time day dealer, play the lengthy sport.

Earlier than I moved states, I had a fairly appreciable checking account.

I wanted that cash in there as a result of I deliberate on placing a down cost on a brand new automotive.

It wasn’t essentially the most financially savvy transfer for a 26-year-old, however it’s not like preserving my cash in financial savings accounts would do me a lot better. In spite of everything, the automotive is an funding in my life.

And, fortunate me, vehicles are literally appreciating proper now, so in a means, I made a sound funding and even acquired a low-interest charge on it, so I’m borrowing cash towards inflation.

However, usually talking, investing money or preserving it in a financial savings account is a hedge towards inflation, that means the worth of your {dollars} goes up within the markets vs. down in a checking account.

Nevertheless, lately, is it higher in your money to lose worth to inflation or to the markets?

The purpose is to maintain as a lot money readily available as is a cushty quantity for you, particularly in at the moment’s inventory market local weather.

I don’t imply this actually.

Finance gurus hate Starbucks, Espresso Bean, and virtually each espresso store due to the markup.

To be truthful, although, whereas the markup of espresso is a giant one, I am going to the native espresso store and snag a medium nitro chilly brew for $3.95.

I might purchase many dearer issues like designer clothes, a extra luxurious automotive, or weekly steak dinners. A espresso prices a couple of bucks, and it makes me pleased, so I’m keen to deal with myself often.

Severely, I deal with myself to a espresso to inspire myself to get away from bed and begin my day. The morning espresso units the tone for the remainder of the day, and low is a excessive ROI buy.

It offers me vitality, and it tastes good.

The underside line: not each seemingly ineffective buy is an irresponsible one. Yeah, you’ll be able to and may make espresso from dwelling because it’s less expensive over the long term, however there’s one thing to be stated in regards to the easy issues.

You virtually at all times deserve a marked-up cup of espresso.

Thoughts your purchases. If a few coffees every month can match comfortably in your price range, do what you need.