Buying a home is an expensive decision and one that can be quite stressful, with home prices that seem to have no ceiling and a purchasing process that can confound even the savviest buyer.

Still, 75% of Americans say buying a home is a priority, according to a new NerdWallet survey conducted online by Harris Poll.

For this report, NerdWallet analyzed data from that December 2017 survey of more than 2,000 U.S. adults, as well as the NerdWallet mortgage calculator, the Consumer Financial Protection Bureau and other sources to develop a snapshot of current home buyer sentiments, concerns and outlooks.

The costs of purchasing a home are a top concern for Americans who rent, and most of those who prefer renting cite financial reasons for their decision, according to the survey. Cost concerns are understandable, with the median price of existing single-family homes climbing 5.3% over the past year, according to the National Association of Realtors.

But these financial concerns aren’t putting a hard stop on sales — approximately 15% of Americans report having purchased a home in the past five years, and 32% intend to do so in the next half-decade. Both of these groups — recent and prospective buyers — are optimistic, citing the investment potential of their home as a top reason for purchasing, according to the survey. Further, data from NerdWallet’s mortgage calculator indicate users anticipate putting a healthy 20% down on their homes.

The survey results also indicate millennials (ages 18-34) aren’t counting themselves out of homeownership — they prioritize homebuying at rates higher than other generations, contrary to the misconception they’re uninterested in putting down roots.

But the news isn’t all positive: Results suggest some Americans aren’t fully informed about the value and costs of homeownership. Some believe buying is more affordable than renting, and while this could be true, especially over the long term, they may not be taking ongoing costs like maintenance, property taxes and homeowners insurance into full consideration. In addition, more than half of Americans indicate they’d rather have an appreciating home than more money in their retirement savings, a potentially dangerous tendency if they’re otherwise ill-prepared to retire comfortably.

“The entry costs to homeownership, such as the down payment and closing costs, can be substantial, but it doesn’t end there,” says NerdWallet mortgage expert Tim Manni. “Prospective home buyers cannot neglect the ongoing costs of ownership when determining how much home they can afford. While your home is likely to be your largest financial asset, and you want to do all you can to make that asset grow, you shouldn’t neglect your other fiscal responsibilities — things like saving for retirement and putting money aside in an emergency fund.”

Key findings

-

Nearly one-third (32%) of Americans plan on purchasing a home within the next five years, and 15% of Americans have purchased one within the past half-decade. Both groups cite “it will be a good investment” as their motivation for buying over all other reasons.

-

The most common reason Americans prioritize buying a home, across all generations, is that they believe it’s a good investment — 64% of those who prioritize it cite this reason.

-

NerdWallet mortgage calculator data indicate potential buyers are being ambitious with their savings goals — intending to put approximately 20% down, on average.

-

Just 17% of Americans say they prefer renting over homeownership, and many of their reasons suggest their choice is out of financial necessity rather than preference. More than half (56%) who prefer renting over buying say they don’t have the money to buy, 24% say they don’t want the financial commitment, and 22% say they have bad credit.

-

82% of millennials (ages 18-34) say buying a home is a priority, according to the survey, compared with 75% of Generation X (35-54) and 69% of baby boomers (55 and older). Millennials also aspire to buy a greater number of homes, on average, throughout their lifetime and are most likely to say they’d like to buy a home to rent out for extra income.

2018 buyer sentiment

Despite strong opinions voiced in 2017 in the media, and likely across dinner tables, about the current economy and political climate, Americans are evenly split on how these factors would influence a 2018 home purchase. When asked whether the current economic and political climate would make them more or less likely to buy a home this year, 35% said more likely, 35% said less likely and 30% said they were unsure.

Considering their overall ability to purchase a home, including finances and housing availability, half (50%) of Americans feel neither better nor worse about their ability to purchase a home this year compared with last year. Of the 28% who feel better, 45% say it’s because they have more in savings and 41% because they have more income. Of the 23% who feel worse, 57% cite having less income and 48% noted less in savings.

Click here to see why Americans feel better or worse about their homebuying abilities.

Homebuying outlook

Approximately one-third (32%) of Americans plan to purchase a home in the next five years. Millennials are most likely to have such a purchase in their five-year plan (49%), versus 35% of Generation X and 17% of baby boomers.

The reasons for purchasing a home are many, and hardly new. “It’s the next step in my life” is the most common reason cited among millennials planning to purchase and those who have purchased in the past five years. Across all generations, and for both prospective and recent buyers, investment potential is also a top motivator.

Rent vs. buy

Thirty-five percent of Americans report they’re currently renting their primary residence, according to the survey, but just 17% say they prefer renting to owning, regardless of their current living situation. Some of the most common answers to why they prefer being a tenant are financial, indicating their choice may be out of necessity rather than preference.

One-third (33%) of Americans who prefer renting say it’s because renting is more affordable. However, not everyone agrees. Nearly as many Americans (30%) who plan on buying a home within the next five years say they will buy because it’s more affordable than renting, and close to the same proportion (26%) of Americans who have purchased a home in the past five years cite this reason.

Home buyer takeaway: The decision to buy a house or continue renting isn’t an easy one. It can be just as emotional as financial. A rent vs. buy calculator can help you weigh the financial side of things, at least. As you’re considering, remember that this isn’t a lifelong decision. Owning a home should be seen as a long-term commitment, for sure, but the right choice now could be different from the right choice in five years. If you opt to keep renting, use this time to pad your savings account and improve your credit, and revisit your decision down the line.

“Some people think that renting is essentially ‘throwing money away’ since ‘you’re not getting anything in return.’ I don’t ascribe to that way of thinking,” Manni says. “Renting allows people flexibility. It gives them the opportunity to live in areas, like big cities, where single-family homes are scarce. But most important of all, renting gives prospective home buyers ample time to save up for a down payment, to resolve credit issues and improve credit scores, and to think long and hard about the type and location of the home you will be ultimately interested in one day.”

Homebuying concerns

The overwhelming majority of Americans (91%) would like to own at least one home in their lifetime, but 88% of current renters have concerns about purchasing one.

Many of those concerns have merit.

Cost

Unsurprisingly, cost is the top renter concern about homebuying. From 2016 to 2017, the median price of existing single-family homes in the U.S. climbed 5.3%, according to the National Association of Realtors. Over that one year, prices rose more than 10% in 19 of 177 metro areas, NAR reports, and prices fell in just 15 metros. Of those 15 metro areas that experienced a drop in home prices, seven saw declines of 1% or less.

Down payment

A big part of the cost of homebuying is the down payment. The 2017 NerdWallet Down Payment Reality Report found 44% of Americans believe you need to have a down payment of 20% or more of the purchase price, and NerdWallet users seem to agree. In 2017, consumers who used NerdWallet’s mortgage calculator — and then clicked away to a mortgage lender’s application site — eyed a 20% down payment, on average. Perhaps unsurprisingly, estimated purchase price and down payment percentage both rose with higher user FICO scores.

Home buyer takeaway: Saving up for a bigger down payment is savvy — it can save you from borrowing as much and paying private mortgage insurance, meaning lower monthly payments. However, putting 20% down isn’t required in today’s market. There are loan options out there that allow as little as 3% down. Know your options. While saving up for a big down payment can pay off in the long term, loans that allow you to put less down could make you a homeowner a lot sooner.

Home maintenance

Maintaining a home is something tenants don’t have to worry about, but it’s an ongoing expense for homeowners, something that 58% of current renters with homebuying concerns recognize. Just how much goes into maintaining a home depends on a variety of factors including region, age of home and condition. In general, homeowners can expect routine and preventive maintenance to equal 1% to 2% of their home’s value annually — for the median price home, at $254,000, that’s roughly between $2,500 and $5,000 each year.

Qualifying for a mortgage

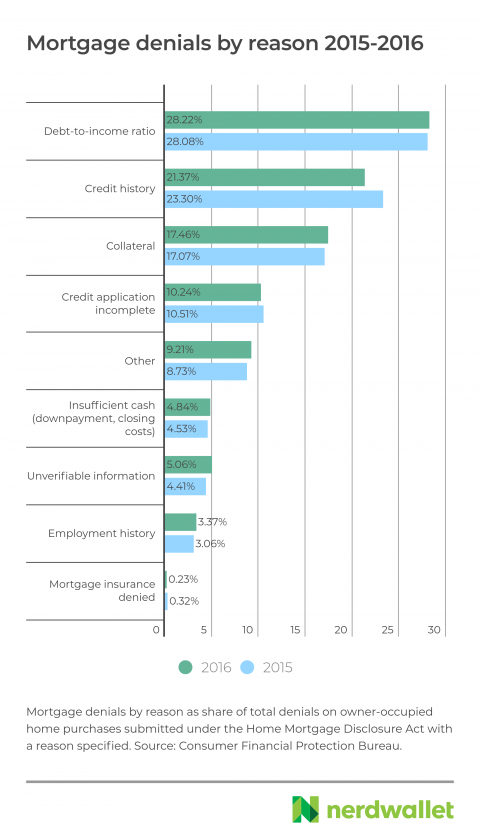

Of those renters with homebuying concerns, 38% are worried about qualifying for a mortgage. According to the most recent data filed under the Home Mortgage Disclosure Act, there were nearly 600,000 mortgage denials in 2016. As in 2015, debt-to-income ratio was the top listed reason for loan denials, followed by credit history.

Home buyer takeaway: If qualifying for a mortgage is your top concern when it comes to buying a home, there are steps you can take now to reduce your debt-to-income ratio and improve your credit — two of the top reasons for mortgage denials. These two goals can take years to achieve, so it’s best to start as you begin amassing your down payment funds.

The mortgage application process

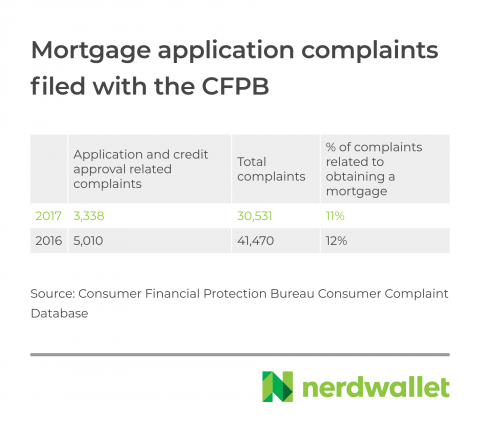

Of renters with homebuying concerns, 28% are concerned about the mortgage application process itself — understandable, considering the time and effort involved. In the 2017 version of this NerdWallet report, 42% of homeowners called the buying process stressful. But home buyers have more options than ever before on how to apply for and navigate the mortgage process. In addition to offering online applications, some lenders even retrieve documents and asset information for you, like Quicken Loans through its Rocket Mortgage interface. Still, some would-be buyers encounter frustrations in the application process that are considerable enough to file formal complaints.

According to NerdWallet analysis of data from the Consumer Financial Protection Bureau, there were some 3,338 complaints filed with that agency related specifically to the mortgage application or underwriting processes in 2017. Most complaints against mortgage lenders fall into the categories of loan servicing, payments, modification and collection, but thousands are directly related to getting a mortgage in the first place.

The CFPB declined to speculate why the total number of complaints fell by 26% from 2016 to 2017.

Homeownership aspirations

Three-fourths (75%) of Americans say buying a home is a priority, and that includes 82% of millennials. Not only does the youngest generation prioritize homebuying at a higher rate than other generations (75% of Generation X and 69% of baby boomers), they also aspire to buy a greater number of homes over time.

Click here to see why Americans prioritize buying a home.

Homebuying as an investment

The most common reason Americans prioritize buying a home, across all generations, is that they believe it’s a good investment — 64% of those who prioritize it cite this reason. Investment value is also the top cited reason recent buyers purchased homes within the past five years (40%), and why prospective buyers want to purchase within the next five years (44%).

More than half (52%) of Americans agree with the statement “I would rather have a home I own appreciate (increase) in value than have more money in retirement savings.” For millennials, it’s 56%, compared with 51% of Generation X and 49% of baby boomers. Additionally, millennials are more likely to want to own a home they can rent out (59%) than Generation X (42%) or baby boomers (20%).

“The goal of every homeowner is to one day sell your house for more than you paid for it. And there are a number of things homeowners can do to help boost their value,” Manni says. “But before you start sinking extra income into your home, be sure you’re also contributing to retirement and your emergency fund has at least a three-month reserve.”

As seen below, individuals with higher annual household incomes are typically less likely than others to see real estate as the best investment option.

Click here to see sentiments around home buying as an investment, by generation.

The 2018 Home Buyer Report’s survey was conducted online within the United States by Harris Poll on behalf of NerdWallet from Dec. 7-11, 2017, among 2,165 U.S. adults ages 18 and older. This online survey is not based on a probability sample and, therefore, no estimate of theoretical sampling error can be calculated.

For additional data and complete survey methodology, including weighting variables and subgroup sample sizes, please contact Maitri Jani at [email protected].

NerdWallet defines generations in the following manner: Millennials, ages 18-34; Generation X, ages 35-54; and baby boomers, age 55+.

Denial reasons in “Mortgage denials by reason 2015-2016” are percentages of the total number of denials for owner-occupied home purchases reported under the Home Mortgage Disclosure Act with a reason stated. Source: Consumer Financial Protection Bureau.

Third-quarter 2017 median home price ($254,000) from the National Association of Realtors.

CFPB mortgage complaint data accurate as of Jan. 17, 2018. Mortgage complaint categories from the agency changed from 2016 to 2017. Those included in the application and credit approval process numbers above include the “application, originator, mortgage broker” and “credit decision/underwriting” categories in 2016 and the “application, originator, mortgage broker,” “applying for a mortgage,” “applying for a mortgage or refinancing an existing mortgage,” and “credit decision/underwriting” categories in 2017.

NerdWallet potential mortgage borrower data pulled from user final entries in the NerdWallet Mortgage Calculator before navigating away to lender websites in all of 2017. Scores below 700 points were grouped together to account for smaller sample sizes.