proceed current profitable streak in Q3 FY26?")

")

IP Galanternik D.U./E+ via Getty Images

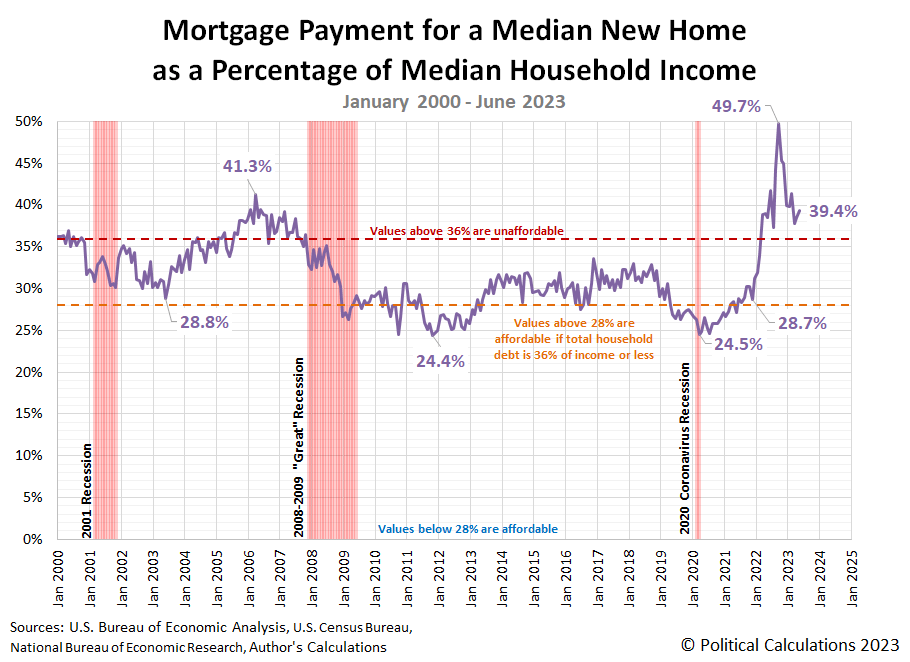

If the typical American household was out looking for an affordable new home to buy in June 2023, they almost certainly didn’t find it.

By typical American household, we’re referring to one that earns the median household income in the United States who, hypothetically, is looking to buy a new home at the median price for which one sold during June 2023.

We say hypothetically because, with the average mortgage rate in the U.S. rising to average 6.71% during the month, the mortgage payment for the median new home sold remained well above the thresholds of affordability.

The following chart shows how May 2023’s relative affordability fits among the data for the 21st century to date:

How bad is it? ATTOM’s report on overall home affordability in the U.S. for the second quarter of 2023 confirms the country faces an affordability crisis:

ATTOM, a leading curator of land, property, and real estate data, today released its second-quarter 2023 U.S. Home Affordability Report showing that median-priced single-family homes and condos are less affordable in the second quarter of 2023 compared to historical averages in 98 percent of counties around the nation with enough data to analyze, continuing a pattern dating back to early 2022.

The report shows that affordability has worsened across the nation this quarter amid a renewed jump in home prices that has pushed the typical portion of average wages nationwide required for major home-ownership expenses up to 33 percent.

We’ll interject here to note that ATTOM is looking at home sales of all types, not just new homes as we are. In addition, average household income is higher than median household income, where 33% of that figure is elevated but falls within a range that most lenders would describe as manageable, provided the household’s overall debt consumes less than 36% of its income.

Because they’re following a different datastream, we found the following discussion of historical home affordability according to their metrics useful for comparison:

Among the 574 counties analyzed, 565, or 98 percent, are less affordable in the second quarter of 2023 than their historic affordability averages. That is slightly higher than the 96 percent level of a year ago and well above 40 percent in the second quarter of 2021. Historical indexes have worsened quarterly in 94 percent of those counties, helping to drop the nationwide index to its lowest point since 2007.

In other words, many of the patterns we’re observing with new homes are applying for the overall U.S. real estate market. One of the main differences is that the shortage of existing homes for sale across the U.S. is contributing to the rapid escalation of their prices when compared to the trend for new homes.

References

U.S. Census Bureau. New Residential Sales Historical Data. Houses Sold. [Excel Spreadsheet]. Accessed 26 July 2023.

U.S. Census Bureau. New Residential Sales Historical Data. Median and Average Sale Price of Houses Sold. [Excel Spreadsheet]. Accessed 26 July 2023.

Freddie Mac. 30-Year Fixed Rate Mortgages Since 1971. [Online Database]. Accessed 26 July 2023. Note: Starting from December 2022, the estimated monthly mortgage rate is taken as the average of weekly 30-year conventional mortgage rates recorded during the month.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.