Q2 2025 Earnings Name Transcript")

proceed current profitable streak in Q3 FY26?")

")

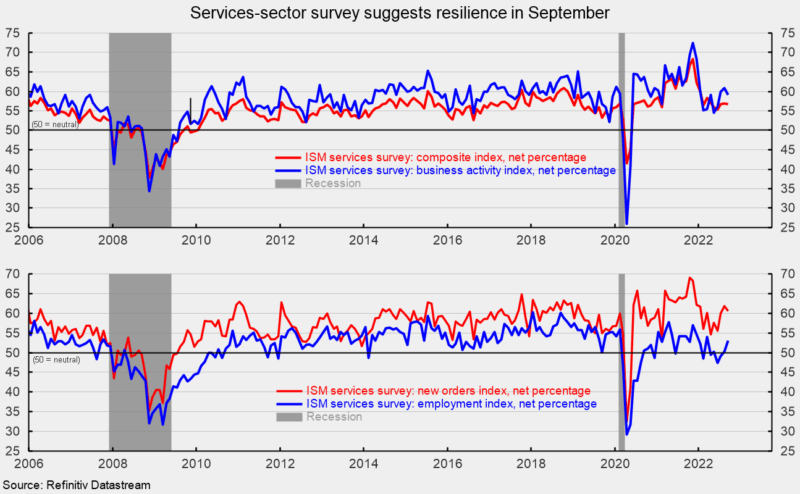

The Institute for Supply Management’s composite services index decreased to 56.7 percent in September, falling 0.2 points from 56.9 percent in the prior month. The index remains above the neutral 50 threshold and suggests the 28th consecutive month of expansion for the services sector (see top of first chart). The September results are very close to the average results for the six years ending December 2019 before the lockdown recession. For the composite index, the average over that period is 56.6 percent.

Among the key components of the services composite index, the business activity index fell 1.8 points to 59.1 (see top of first chart). That is the 28th month above 50, and 0.7 percentage points below the six-year average of 59.7 percent. Fourteen industries reported increased activity while two reported slower activity.

The services employment index improved in September, coming in at 53.0 percent, up from 50.2 percent in August. That is just the fourth time in the last eight months that the employment index was above neutral, with an average of 50.2 percent over that period (see bottom of first chart). The September result is also below the six-year average (2014-2019) of 55.1 percent.

Ten industries reported employment growth, while two reported a reduction. Respondents suggest qualified labor continues to be in short supply, but several noted somewhat easier labor conditions.

The services new-orders index fell to 60.6 percent from 61.8 percent in August, decreasing by 1.2 percentage points (see bottom of first chart). The new orders index has been above 50 percent for 28 consecutive months and is 1.7 points above the six-year average of 58.9 percent.

The nonmanufacturing new-export-orders index, a separate index that measures only orders for export, improved in September, coming in at 65.1 versus 61.9 percent in August. Six industries reported growth in export orders, with three reporting declines and nine reporting no change. However, for all respondents, only about 23 percent said they perform and track separate activity outside the US.

Backlogs of orders in the services sector likely grew again in September though the pace likely decelerated as the index decreased to 52.5 percent from 53.9 percent. September was the 21st month in a row with rising backlogs. Ten industries reported higher backlogs in September, while four reported decreases.

Supplier deliveries, a measure of delivery times for suppliers to nonmanufacturers, came in at 53.9 percent, down from 54.5 percent in the prior month (see top of second chart). It suggests suppliers are falling further behind in delivering supplies to services business, but the slippage has decelerated from the prior month. The index has moved sharply lower since back-to-back readings above 75 in October and November 2021, and is at the lowest level since February 2020, just before the lockdown recession. The manufacturing sector survey matches the recent improvement (see top of second chart). For the services sector, ten industries reported slower deliveries in September while six reported faster deliveries.

The nonmanufacturing prices paid index fell to 68.7 percent in September, the fifth consecutive decline from a record-high 84.6 percent in April (see bottom of second chart). Eighteen industries reported paying higher prices for inputs in September. Price pressures have eased somewhat for the services sector while the manufacturing sector has seen a significant decline in price pressures (see bottom of second chart).

The latest Institute of Supply Management report suggests that the services sector and the broader economy expanded for the 28th consecutive month in September. Respondents to the survey continue to highlight ongoing input price pressures, as well as materials and labor shortages though some of the respondents noted some signs of improvement. Respondents also reported signs of easing demand and concern about the economic outlook.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals.

Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.