")

")

")

")

By Lance Roberts

“Geopolitical Threat” might nicely be a cause for the Fed to slow-roll tightening financial coverage in March. With Russia invading Ukraine, such wouldn’t be the primary time that the Fed used “geopolitical threat” to stay cautious on adjustments to financial coverage.

“Weak world demand and geopolitical dangers additionally argue for going sluggish, Mr. Powell stated, in addition to a decrease long-run impartial federal-funds fee and the “apparently elevated sensitivity to monetary situations to financial coverage.” – WSJ, Could 2016

In 2018, the Fed was climbing charges and tapering their stability sheet. Then, with the market beneath duress, rising geopolitical dangers with China started to melt the Fed’s extra hawkish stance. Not lengthy after, the Fed began chopping charges and bailed out hedge funds by an “unofficial QE” program. That was all earlier than the 2020 “pandemic-shutdown” bailout of every part.

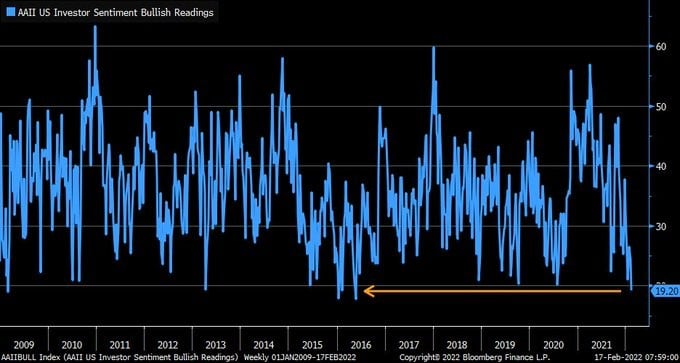

Whereas the Fed suggests it would hike charges at its March assembly to fight present inflation, they face a number of challenges from falling client confidence, weak markets, and really bearish investor confidence. It wasn’t stunning to see Fed member Mary Daly recommend the FOMC “should navigate geopolitical uncertainty.”

*DALY: FED MUST NAVIGATE GEOPOLITICAL UNCERTAINTY GOING FORWARD

setting stage for fewer fee hikes/fee cuts

— zerohedge (@zerohedge) February 23, 2022

With markets sliding and traders extra bearish than in 2016, simply earlier than world central banks went “full QE” to offset Brexit, the Fed is now confronted with “monetary instability.”

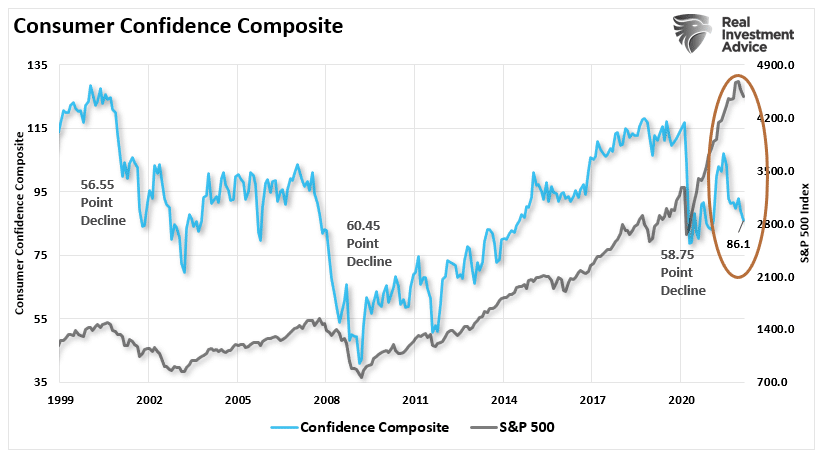

The fallout of the present Russia/Ukraine standoff will not be solely impacting markets however undercutting client confidence as nicely.

The Shopper Confidence Key

Within the U.S., shoppers drive 70% of financial development. Such is why “value stability” is so essential to the Fed.

To grasp why confidence is so very important, we have to revisit what Ben Bernanke stated in 2010 as he launched the second spherical of QE:

“Simpler monetary situations will promote financial development. For instance, decrease mortgage charges will make housing extra reasonably priced and permit extra householders to refinance. Decrease company bond charges will encourage funding. And better inventory costs will enhance client wealth and assist enhance confidence, which may additionally spur spending.”

The issue is the economic system is not a “productive” one however quite a “monetary” one. A degree made by Ellen Brown beforehand:

“The financialized economic system – together with shares, company bonds and actual property – is now booming. In the meantime, the majority of the inhabitants struggles to fulfill every day bills. The world’s 500 richest individuals received $12 trillion richer in 2019, whereas 45% of People don’t have any financial savings, and practically 70% couldn’t provide you with $1,000 in an emergency with out borrowing.

Central financial institution insurance policies supposed to spice up the true economic system have had the impact solely of boosting the monetary economic system. The insurance policies’ acknowledged goal is to extend spending by rising lending by banks, that are speculated to be the automobiles for liquidity to movement from the monetary to the true economic system. However this transmission mechanism isn’t working, as a result of shoppers are tapped out.”

If consumption retrenches, so does the economic system.

The issue for the Fed is that client confidence is already declining, tightening financial coverage will exacerbate the decline.

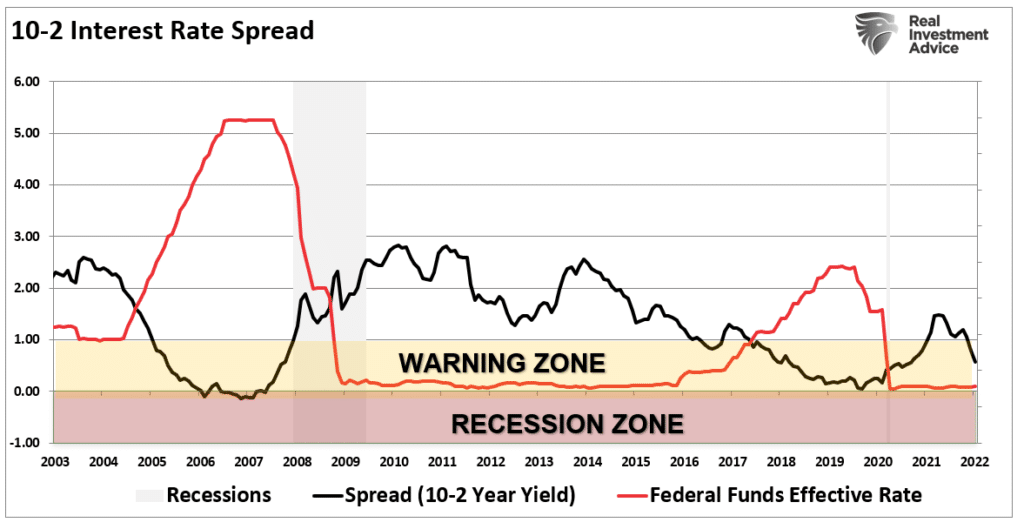

However it isn’t simply client confidence that’s an issue. The ahead yield curve suggests the Fed is already trapped.

The Ahead Yield Curve

Some of the correct indicators of the onset of a recession is an “inversion” of the yield curve. As famous in Potemkin Economic system:

“Probably the most vital threat is the Fed turning into aggressive with tightening financial coverage to the purpose one thing breaks. That concern will present itself as a disinflationary impulse that pushes the economic system in the direction of a recession. The yield curve could also be telling us this already.”

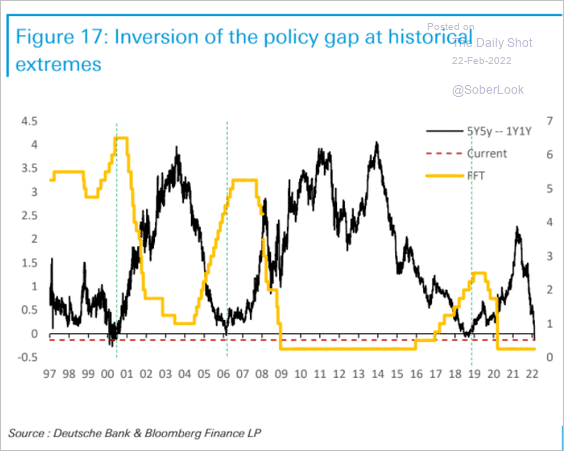

Whereas the yield curve suggests the economic system is already weakening, a distinct yield curve suggests the Fed could also be too late. The chart beneath reveals the distinction in yields between the 5-year and 1-year ahead yields. This specific yield curve signifies that deflation and financial weak spot will arrive over the 12-months.

Importantly, word that when this “ahead” yield curve turns into inverted, the Fed was near a peak of their fee climbing cycle. The plain downside is that the ahead yield curve is inverted, and charges stay at zero.

The Fed has little room for error between an inverted ahead curve, declining client confidence, and rising geopolitical threat.

Whereas they’ll attempt to hike charges, we suspect they’ll wind up “breaking one thing.”

Historical past Suggests The Fed Will Make A Mistake

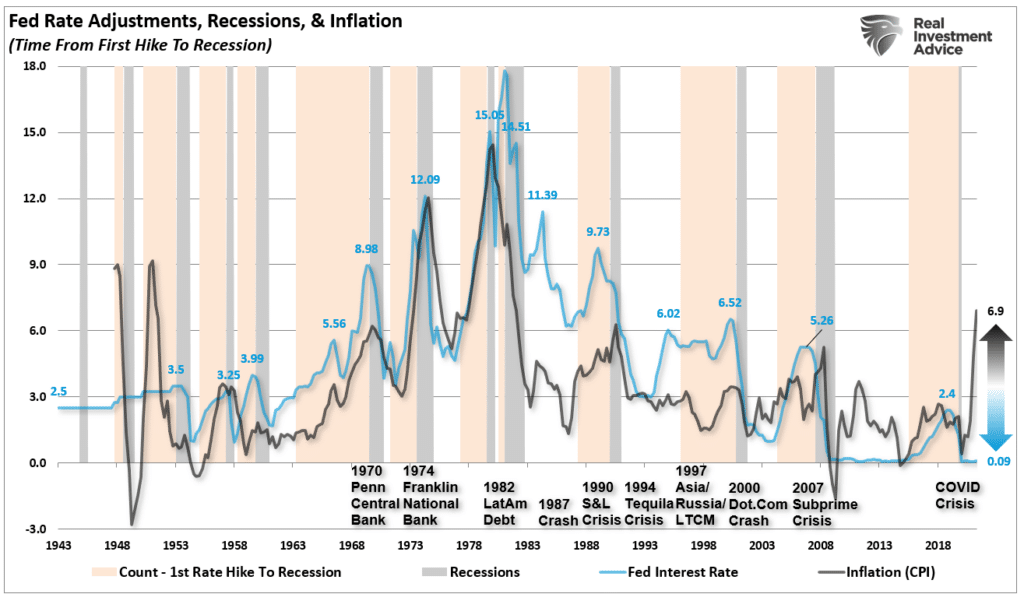

Since 1980, each time the Fed tightened financial coverage by climbing charges, inflation remained “nicely contained.” The chart beneath reveals the Fed funds fee in comparison with the patron value index (CPI) as a proxy for inflation.

There are three important factors within the chart above.

- The Fed tends to hike charges together with inflation, to the purpose it “breaks one thing” out there.

- For almost all of the final 30-years the Fed has operated with inflation averaging nicely beneath 3%.

- The present unfold between inflation and the Fed funds fee is the biggest on file.

Traditionally, the Fed hiked charges to fight inflation by slowing financial development.

Nonetheless, this time the Fed is climbing charges after short-term fiscal stimulus pulled-forward demand, creating a synthetic inflation surge.

Importantly, lots of these disaster factors had been credit-related. With debt and leverage close to historic excessive ranges, rising rates of interest inevitably causes an issue. As Former Fed Governor Randall Kroszner beforehand stated:

“The massive money owed that governments are racking up are going to make it troublesome for central banks to boost charges after they really feel the necessity to take action as a result of that can enhance borrowing prices.”

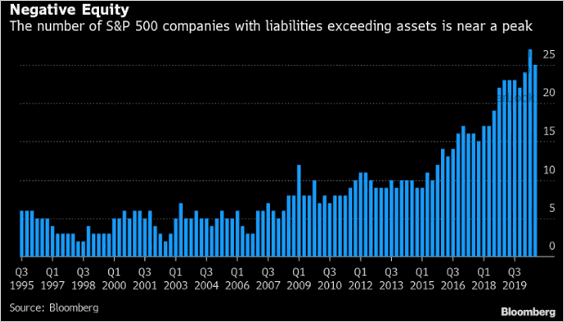

In an economic system laden by greater than $75 Trillion in debt, a file variety of “Zombie” firms stored alive by low borrowing prices, and a near-record variety of firms with destructive fairness, larger charges shall be an issue. The one query is when?

As famous above, the final time that “geopolitical dangers” had been of concern to the Fed was in 2018 and 2019. Presently, the market is mapping out a lot the identical course.

We won’t be shocked to see the Fed soften its place on fee hikes in March for all of those causes.

The 2018 analog could already be telling us the identical.