Run Time: 1H 58M Plus Bonus Jazz!")

")

With the federal debt ceiling fight looming in Congress, now is a good time to look again at how much the federal government owes, and whether the new Republican House majority will be able to keep spending under control.

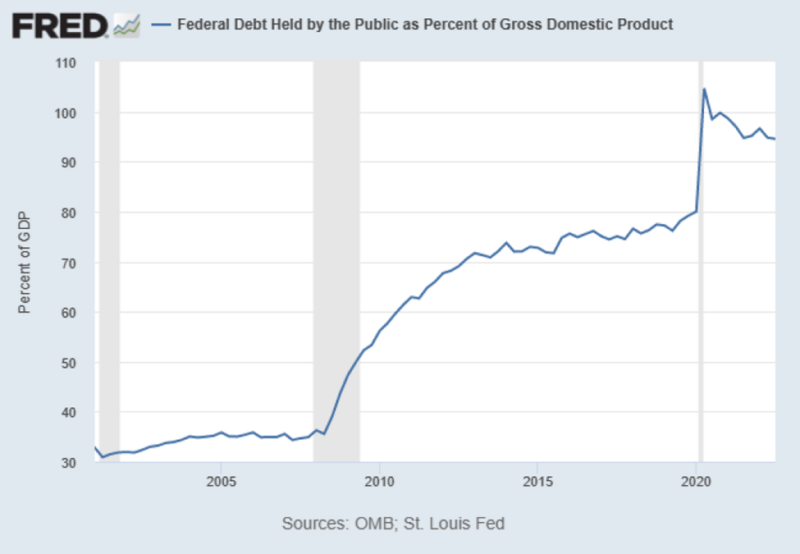

Figure 1 shows how federal debt held by the public as a percentage of the economy has changed between first quarter 2001 and second quarter 2022. Over the last 21 years, federal debt has tripled as a share of the economy. Now, these figures include debt held by the Federal Reserve System; in recent years, excluding that debt would reduce these figures by about 15 percentage points of GDP. But if we want to compare the US to other countries, we would need to include state and local debt, which USgovernmentspending.com “guesstimates” (actual local debt data releases lag by a couple of years) were about $3.5 trillion by mid-2022, or 14 percent of GDP. Thus, general government debt held by private investors in the US almost certainly tops 90 percent of GDP today, which is right around the level in the United Kingdom, above Germany and below Canada and Spain.

Figure 1: Federal Debt Held by the Public, % of GDP, United States

The US is, therefore, probably nearing the limit of what investors would be willing to tolerate. Debt-burdened countries like Spain and Italy owe about 120 percent of GDP. Another spending spree like those of 2009 or 2020 could take this country right to that ceiling. Cutting federal spending is an absolute necessity if we are to avoid significant tax increases in the future.

Will Congress actually cut spending? History suggests not. Economic historian Robert Higgs invented the term “ratchet effect” to describe the way that government growth after a crisis tends to be locked in: the size of government never retreats to what it was before the crisis.

To answer this question more definitively, I revisit here some research I did in December 2016 and see if my conclusions have held good for the past few years. If so, we can have more confidence that there is a causal relationship between divided government and spending restraint. This is what econometricians call “out-of-sample prediction.”

At the end of 2016, Republicans were about to take full control of the federal government. I hypothesized that in the first year of unified partisan control, Congress would increase spending on the priorities of the party in power, but I did not expect that they would continue to increase spending at an unusually fast rate in subsequent years. In other words, every time there was a transition to unified party control of the federal government, spending would rise rapidly, but in other years, there would be no difference in spending growth between divided government and unified government. I used inflation-adjusted data on federal budgeted and actual spending growth rates from fiscal year 1977 to 2016 to test my hypothesis, and the data supported it.

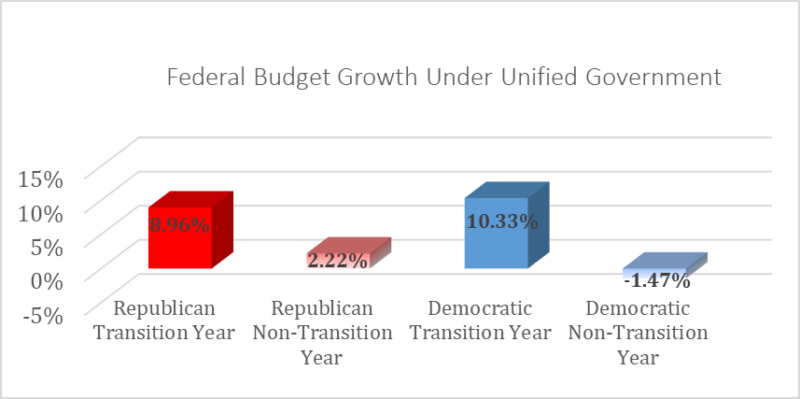

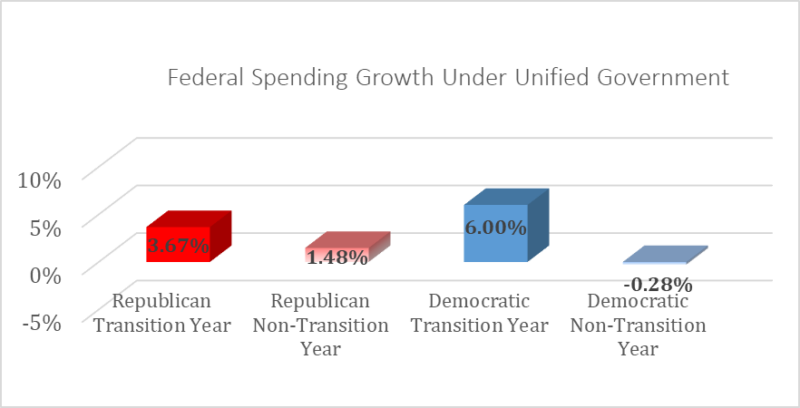

Figures 2 and 3 show the estimated statistical effect of a unified federal government in its first and subsequent years on budgeted and actual spending, respectively.

Figure 2: Predicted Budget Growth Rates Under Unified Democratic and Republican Control, Relative to Divided Government

Figure 3: Predicted Spending Growth Rates Under Unified Democratic and Republican Control, Relative to Divided Government

The data revealed that under the first year of unified Republican control, Congress had budgeted nine percentage points more spending compared to a divided government year. In subsequent years, Congress had budgeted only two percentage points more spending compared to a divided government year. Democrats budgeted over 10 percentage points more spending in their first year of control, but actually might have spent a little less in subsequent years than under divided government. The figures were more moderate for actual compared to budgeted spending.

Did my prediction hold good for transitions to unified Republican control in 2017 and unified Democratic control in 2021?

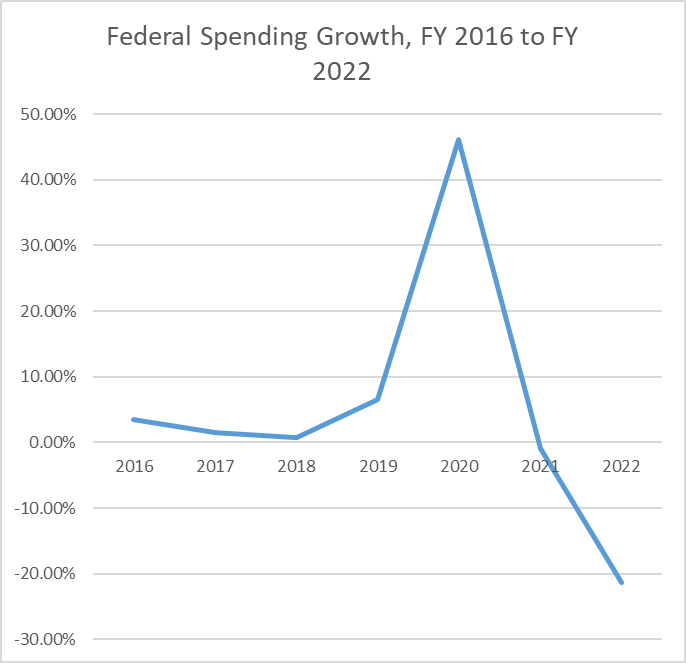

Only in part. Figure 4 shows the annual, inflation-adjusted percentage change in federal spending from fiscal year 2015 to fiscal year 2022, according to U.S. budget documents. Republicans increased federal spending less under unified control in fiscal year 2017 than the divided government had in fiscal year 2016, but they increased it even less in their second year of control. Then federal spending grew faster under divided government during and after the 2018 midterm election season and exploded in 2020 because of COVID-19. This evidence certainly does not suggest that divided government restrains spending, but it does imply that unified government increases it more rapidly in their first year of control.

Finally, under unified Democratic control federal spending was steady in FY 2021, and then declined rapidly in FY 2022 as the COVID-19 stimulus subsided. The decline in federal spending in FY 2022, however, was not nearly enough to make up for the explosion in FY 2020, and the fact that federal spending got locked in at an apparently permanently much-higher level is, itself, a sort of evidence for the unified-government-transition hypothesis.

Figure 4: Annual Rate of Growth in Federal Spending, FY 2015 to 2022

To sum up, we shouldn’t expect a transition from unified Democratic control to divided government to reduce the rate of growth in federal spending. The evidence from before 2016 suggests that divided government restrained spending only compared to years in which there was a transition to unified government. The evidence since 2016 is even less positive about divided government, because divided government increased spending abnormally rapidly in 2015 and 2016 and then again in 2019 and 2020.

The Republican House will probably shift spending somewhat from Democratic to Republican priorities, but if Democrats or Republicans take full control of DC after the 2024 election, they will, more likely than not, increase spending on their priorities without cutting what’s already been “baked in” to the federal budget. The ratchet effect lives on, and divided government can only delay growth in government, not reverse it.

Jason Sorens

Jason Sorens, Ph.D., is Senior Research Faculty at AIER. He was formerly the director of the Center for Ethics in Business and Governance at Saint Anselm College. He has researched and written more than 20 peer‐reviewed journal articles, a book for McGill‐Queens University Press titled Secessionism, and a biennially revised book for the Cato Institute, Freedom in the 50 States (with William Ruger).

His research has focused on fiscal federalism, U.S. state politics, and movements for regional autonomy and independence around the world. He has taught at Yale, Dartmouth, and the University at Buffalo and twice won awards for best teaching in his department. He lives in Manchester, New Hampshire.